Are Banks In Trouble, and what does it mean for you? Bankprofits.net dives deep into the financial health of banks, offering insights into bank profitability and stability strategies to help you understand the current state of the banking sector. Discover how factors like interest rates, deposit levels, and regulatory changes impact bank performance and what measures are being taken to ensure financial stability.

1. Understanding the Current Concerns About Bank Stability

Are banks in trouble? Yes, recent failures and economic conditions have created concerns. Bank failures, unrealized investment losses, and reliance on uninsured deposits are raising concerns about the overall health of the banking industry. Let’s delve into the factors contributing to these anxieties and explore the steps being taken to address them.

Several key elements contribute to the current concerns about bank stability:

- Past Bank Failures: The failures of Silicon Valley Bank and Signature Bank in 2023 eroded public confidence and revealed vulnerabilities in risk management.

- Interest Rate Impact: Rising interest rates can diminish the value of bank assets, particularly long-term investments, leading to financial strain.

- Uninsured Deposits: Banks with a high proportion of uninsured deposits are more vulnerable to sudden withdrawals, potentially triggering a liquidity crisis.

- Economic Uncertainty: Broader economic uncertainties can impact loan performance and investment returns, adding pressure to banks’ financial health.

2. Are 186 Banks Really at Risk of Failure?

Are banks in trouble to the point of failure? A recent report suggested nearly 186 banks could be at risk due to rising interest rates and high uninsured deposits. Let’s examine this report and its potential impact.

According to a report from the Social Science Research Network, a significant number of banks may be vulnerable due to:

- Rising Interest Rates: The Federal Reserve’s rate hikes have reduced the market value of bank assets.

- Uninsured Deposits: A large percentage of deposits exceeding the FDIC insurance limit of $250,000 makes banks susceptible to rapid withdrawals.

The report indicated that if just half of uninsured depositors withdrew their funds, approximately 186 banks could face impairments, potentially endangering around $300 billion in insured deposits. This scenario highlights the critical importance of risk management and diversification in bank funding.

3. Examining the FDIC’s “Problem Bank” List

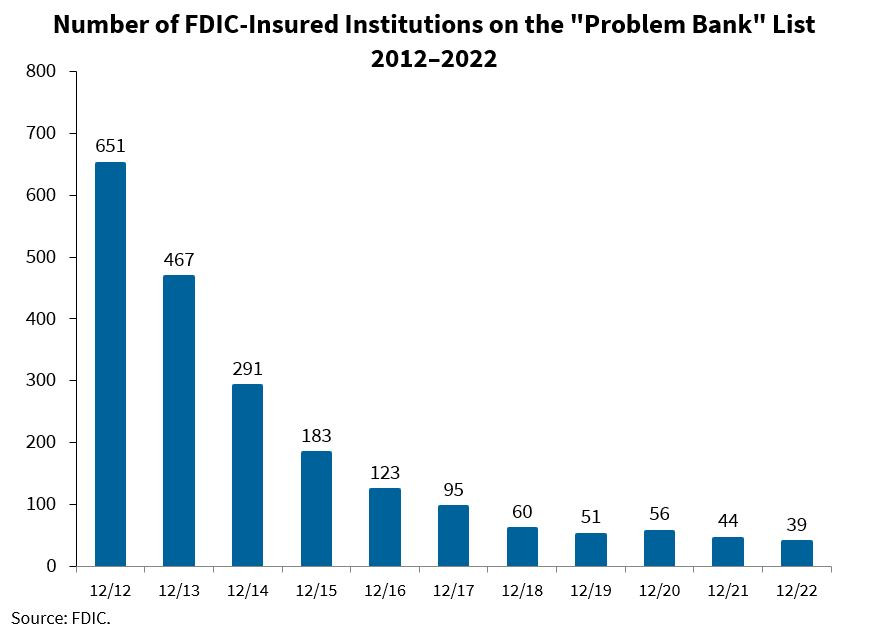

Are banks in trouble according to official regulators? The FDIC’s “Problem Bank” list is a key indicator. This list tracks banks with financial, operational, or managerial weaknesses. While the number of banks on this list has decreased over the years, it’s essential to understand what this list signifies.

The number of FDIC-insured institutions on the “Problem Bank” list has shown a positive trend, decreasing from 651 in 2012 to 39 by the end of 2022. This decline suggests improvements in the banking sector’s stability and resilience. The FDIC actively monitors these institutions to ensure they address their challenges and comply with regulatory requirements.

| Month/Year | Number of Problem Banks |

|---|---|

| 12/2012 | 651 |

| 12/2013 | 467 |

| 12/2014 | 291 |

| 12/2015 | 183 |

| 12/2016 | 123 |

| 12/2017 | 95 |

| 12/2018 | 60 |

| 12/2019 | 51 |

| 12/2020 | 56 |

| 12/2021 | 44 |

| 12/2022 | 39 |

FDIC Insured Institutions on the Problem Bank List

FDIC Insured Institutions on the Problem Bank List

4. The Role of CRA Compliance in Bank Stability

Are banks in trouble if they don’t comply with regulations? The Community Reinvestment Act (CRA) is crucial. Banks are regularly examined for CRA compliance, ensuring they meet the credit needs of their communities. Non-compliance can indicate broader issues within the institution.

The FDIC issues a Monthly List of Banks Examined for CRA Compliance, which includes:

- Bank Names: Identifies the institutions under review.

- Examination Dates: Provides a timeline of compliance evaluations.

This list helps regulators, community organizations, and the public monitor banks’ performance in supporting local communities. Banks with assets greater than or equal to $250 million may be examined in advance of the examination mandate date. Banks are examined for CRA compliance every 12 to 36 months, depending on their asset size and rating.

5. What Happens if Banks Fail? Potential Impacts

Are banks in trouble to the point where failures impact the economy? Bank failures can have significant repercussions, potentially leading to credit crunches and economic slowdowns. Understanding these impacts is vital.

If a large number of banks fail, it could lead to:

- Credit Contraction: Businesses and consumers may find it difficult to access credit, hindering economic activity.

- Bank Runs: Depositors may withdraw funds from other banks, causing broader panic and instability in the banking system.

- Economic Recession: A loss of confidence in the banking system can trigger a recession or even a financial crisis.

Government intervention, such as recapitalizing vulnerable banks and providing deposit guarantees, is essential to prevent wider panic and economic disruption.

6. Strategies Banks Can Use to Improve Stability and Profitability

Are banks in trouble and what can they do about it? Banks can employ several strategies to bolster their stability and profitability. These strategies include diversification of funding sources, careful risk management, and proactive adaptation to regulatory changes.

- Diversifying Funding Sources: Reducing reliance on uninsured deposits can mitigate the risk of sudden withdrawals.

- Prudent Risk Management: Accurately assessing and managing risks associated with interest rates and investments is crucial.

- Regulatory Compliance: Adhering to regulatory requirements ensures the safety and soundness of financial operations.

- Technological Innovation: Embracing digital transformation and innovative solutions can improve efficiency and customer service.

By implementing these strategies, banks can enhance their resilience and navigate economic challenges effectively.

7. How Economic Conditions Impact the Banking Sector

Are banks in trouble due to the economy? Economic conditions significantly influence bank performance. Factors like interest rates, inflation, and overall economic growth can affect profitability.

- Interest Rates: Changes in interest rates impact the value of bank assets and the profitability of lending activities.

- Inflation: Rising inflation can erode the real value of assets and increase operational costs.

- Economic Growth: A strong economy typically leads to increased lending and investment activity, boosting bank profits.

Banks must closely monitor these economic indicators and adjust their strategies to maintain stability and profitability.

8. The Role of Technology in Modern Banking

Are banks in trouble if they don’t adapt to technology? Technology plays a pivotal role in modern banking. Digital transformation, fintech innovations, and cybersecurity measures are crucial for staying competitive and secure.

- Digital Transformation: Embracing digital technologies can enhance customer experience, streamline operations, and reduce costs.

- Fintech Innovations: Partnering with fintech companies can offer innovative solutions and expand service offerings.

- Cybersecurity Measures: Protecting against cyber threats is essential for maintaining customer trust and safeguarding financial assets.

Banks that effectively leverage technology can improve efficiency, enhance security, and adapt to changing customer expectations.

9. Regulatory Changes and Their Effects on Banks

Are banks in trouble because of changing regulations? Regulatory changes significantly impact how banks operate. Compliance with new regulations, such as capital requirements and consumer protection laws, is crucial.

- Capital Requirements: Higher capital requirements ensure banks have sufficient resources to absorb losses.

- Consumer Protection Laws: Regulations aimed at protecting consumers can impact lending practices and profitability.

- Financial Stability Oversight: Regulatory bodies monitor systemic risks and implement measures to prevent financial crises.

Banks must stay informed about regulatory changes and adapt their operations to ensure compliance and maintain stability.

10. Expert Opinions: What Financial Analysts Say About Bank Stability

Are banks in trouble according to the experts? Financial analysts offer valuable insights into the stability of the banking sector. Their analysis of financial data, market trends, and regulatory developments provides a comprehensive view of the industry’s health.

- Market Analysis: Experts analyze market trends and financial data to assess the overall health of the banking sector.

- Risk Assessment: Analysts evaluate the risks associated with interest rates, economic conditions, and regulatory changes.

- Industry Outlook: Experts provide insights into the future outlook for the banking industry, highlighting potential challenges and opportunities.

Staying informed about expert opinions can help individuals and businesses make informed decisions about their banking relationships and investments.

FAQ: Addressing Your Concerns About Bank Stability

1. What are the main reasons banks fail?

Banks primarily fail due to poor risk management, insufficient capital, and liquidity problems.

2. How does the FDIC protect depositors?

The FDIC insures deposits up to $250,000 per depositor, per insured bank.

3. What is a “bank run” and why is it dangerous?

A bank run occurs when a large number of depositors withdraw their funds simultaneously, potentially leading to the bank’s collapse.

4. How do interest rates affect bank stability?

Rising interest rates can decrease the value of bank assets and increase borrowing costs, impacting profitability.

5. What role does technology play in bank stability?

Technology enhances efficiency, improves customer service, and helps banks manage risks more effectively.

6. What are the key regulations that govern banks?

Key regulations include capital requirements, consumer protection laws, and financial stability oversight.

7. How can I assess the financial health of my bank?

Review the bank’s financial statements, ratings from independent agencies, and news reports about its performance.

8. What is the Community Reinvestment Act (CRA)?

The CRA requires banks to meet the credit needs of the communities they serve, including low- and moderate-income neighborhoods.

9. How do economic conditions impact the banking sector?

Economic growth, inflation, and interest rates all influence bank lending, investment, and profitability.

10. What strategies can banks use to improve their stability?

Diversifying funding sources, managing risks prudently, and adapting to regulatory changes are crucial.

In conclusion, while concerns about bank stability are valid, understanding the factors at play and the measures being taken to address them is essential. For in-depth analysis, strategies, and up-to-date information on bank profitability, visit Bankprofits.net. Stay informed, stay secure, and make sound financial decisions. Contact us at Address: 33 Liberty Street, New York, NY 10045, United States, Phone: +1 (212) 720-5000, or visit our Website: bankprofits.net for more insights and expert advice.