The traditional landscape of brick and mortar bank branches is undergoing a significant transformation. This disruption presents an opportunity for financial institutions to refine their human capital strategies, enhancing value for both employees and customers.

This article explores how advancements in retail banking are compelling firms to reassess their staffing models, job roles, and established compensation practices for conventional branch positions, with a particular focus on Bank Teller Compensation.

The Shifting Role of Bank Branches

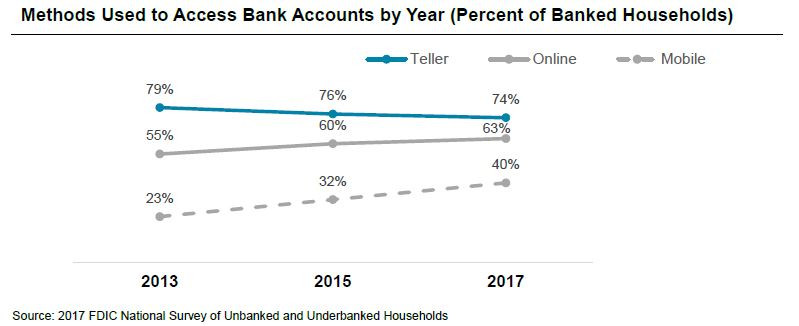

Recent data from the FDIC’s National Survey of Unbanked and Underbanked Households indicates a notable surge in digital account access among U.S. banked households between 2013 and 2017. Interestingly, during the same period, the utilization of bank tellers experienced only a modest decrease. This suggests that while digital banking is on the rise, it hasn’t completely replaced the need for in-person customer service at branches. Consider that bank branches in the U.S. still outnumber Starbucks locations by a factor of six. More significantly, a substantial 74% of banked households still interacted with a teller at least once in 2017. This data underscores an important opportunity for banks to strategically redirect branch activities towards more value-added services within this high-cost physical channel. Branch personnel, especially tellers, remain crucial in influencing bank sales, brand perception, and overall customer experience.

Bank Teller Interactions Remain Significant Despite Digital Growth

Bank Teller Interactions Remain Significant Despite Digital Growth

Reimagining Branch Staffing and Teller Roles

Banks are proactively reshaping the branch experience through innovative formats. These include the adoption of “pods” or workstation layouts instead of traditional teller lines, the creation of café-style branches, and the deployment of smart ATMs as alternatives to human tellers. The 2018 deployment of Pepper the Robot by HSBC in a U.S. branch further exemplifies this trend. These innovations highlight the imperative to rethink branch staffing models and the evolving role of the bank teller.

The traditional teller role, primarily focused on processing over-the-counter transactions, is evolving. Modern teller job descriptions now frequently encompass customer education on banking products, guidance on self-service applications, and efficient problem resolution. This shift is also reflected in job title rebranding. More than 40% of firms participating in the recent McLagan Retail Pay Practices Study utilize titles other than “teller,” such as “service associate/specialist” or “banker.” The “universal banker” concept, a role combining sales and service responsibilities, gained momentum around 2013 with the initial aim of ultimately replacing all teller positions. While a complete transition hasn’t materialized, firms that predominantly employ universal bankers typically see teller headcount reduced by more than half as a proportion of total branch staff.

Branch staffing strategies should be aligned with the bank’s broader retail strategy, while also maintaining adaptability to diverse market needs. Transactional, sales, and advisory opportunities will vary across different branch locations. Consequently, effective training and performance management are essential components of any branch role transformations, including adjustments to bank teller compensation structures.

Modernizing Bank Teller Compensation Strategies

In light of recent market pressures on salary and incentive practices, aligning branch pay programs with evolving role priorities is crucial, particularly in the context of bank teller compensation.

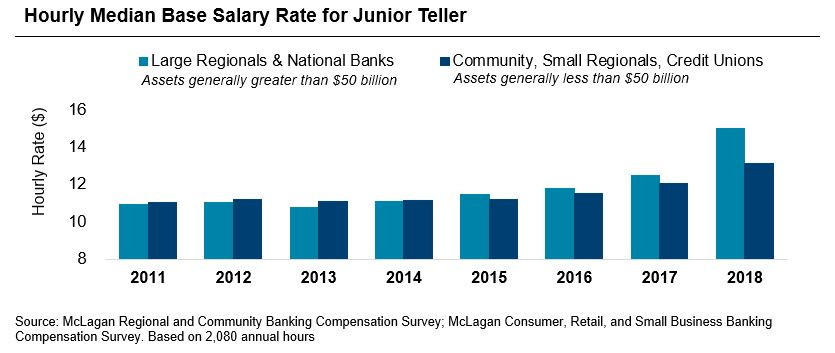

Starting pay became a significant issue in 2018, driven by both the Tax Cuts and Jobs Act of 2017 and increases in city/state minimum wages. Numerous large firms publicly announced minimum wage increases to $15 per hour, creating upward pressure across various industries. McLagan’s 2018 Consumer Compensation Survey revealed a 20% median base pay increase for tellers at large banks, significantly exceeding the historical 3% year-over-year growth. Smaller regional and community banks exhibited less uniform base pay increases, dependent on local labor market conditions. It is important to recognize that banks are not solely competing with other bank branches for teller staff; these skills are transferable to various retail and service sectors. While increasing base salaries can represent a considerable organizational expense, it is vital to balance this cost against the expenses associated with employee turnover and recruitment.

Base Pay Increases for Bank Tellers

Base Pay Increases for Bank Tellers

Raising base pay for branch staff has implications beyond entry-level tellers. Adjusting compensation for senior tellers and other banker roles remains a challenge as firms strive to maintain appropriate salary differentiation. In some instances, the increased fixed costs associated with rising base pay have led firms to eliminate incentive programs for tellers altogether, impacting the overall bank teller compensation package.

Teller incentives, typically representing less than 5% of total pay and often distributed quarterly or monthly, are a relatively small component of bank teller compensation. These incentive plans primarily focus on sales-related activities, such as customer referrals or cross-selling products. The 2016 retail sales practices scandal brought industry-wide scrutiny to branch sales tactics and goal setting, prompting firms to implement stricter governance over sales practices and incentive plans, influencing the design of bank teller compensation programs.

In the 2018 Retail Pay Practices Study, 52% of firms reported adjusting performance measures in branch incentive plans within the preceding year. A shift in focus is evident, moving away from purely referral and transaction-based metrics towards programs that incorporate customer experience, teamwork, compliance, and digital migration. While these broader measures can effectively balance sales and service objectives, their qualitative nature often introduces subjectivity and makes individual-level tracking more complex, requiring careful consideration in bank teller compensation plan design.

Reconsidering Teller Incentive Programs within Bank Teller Compensation

Firms must evaluate whether their bank teller compensation programs, particularly incentive components, effectively drive desired performance and align with evolving role responsibilities. Key considerations surrounding the potential elimination of teller incentive programs include the administrative burden of plan management, relatively high reputational risks associated with aggressive sales targets, small payout amounts that may not effectively motivate behavior, and overall program affordability in the context of total bank teller compensation.

The removal of variable pay elements in bank teller compensation must be counterbalanced with other HR strategies, such as greater differentiation in salary increases, robust employee recognition programs, investments in comprehensive training, and clearly defined career progression pathways. Relying solely on base salary for tellers may also help alleviate salary compression issues, as incentive eligibility can then be used to differentiate total compensation opportunities for more senior roles within the branch network.

Outdated widget-based referral incentive plans for tellers are becoming less relevant. Banks are now prioritizing activities such as customer education and enhancing customer experience, while simultaneously encouraging the migration of transactional activities to lower-cost digital channels. One approach to modifying incentive programs is extending the performance period to semi-annual or annual payouts. This allows for the evaluation of qualitative metrics over a longer timeframe, promotes staff retention, and reduces the administrative time and costs associated with frequent plan administration, thus impacting the structure and delivery of bank teller compensation.

Robust control mechanisms are essential for all incentive plans to detect and address any improper activity. Incentive plan design and administration should involve oversight from control functions outside of the business line, including human resources, finance, and risk/compliance departments, ensuring the integrity of bank teller compensation practices.

Conclusion: Evolving Human Capital Strategy for Bank Tellers

As branch strategies continue to evolve in the digital age, so too must the human capital strategy, especially concerning bank teller compensation. While retail banking is increasingly leaning towards digital transactions, physical branches remain a touchpoint for a majority of customers annually. Therefore, developing an effective HR strategy for tellers, who constitute a significant 40% of branch staff, is of paramount importance.

Key areas for consideration in optimizing bank teller compensation and overall HR strategy:

-

Align Branch Staffing and Roles with Strategic Direction: Determine the firm’s commitment to the teller position – whether to maintain it or transition towards a universal banker model. Appropriate training and development initiatives are crucial for successful branch transformations and should be considered as part of the overall employee value proposition beyond just bank teller compensation.

-

Benchmark Salaries Against Local Competition: Maintain competitive base pay relative to both bank and non-bank competitors in the local labor market. Understand how the firm’s broader value proposition, which may include variable pay, comprehensive benefits, or enhanced career advancement opportunities, attracts and retains talent in addition to bank teller compensation.

-

Evaluate the Effectiveness of Teller Incentive Programs: Focus incentive measures on behaviors that drive the most value for the firm and align with the evolving teller role. If the current plan structure is misaligned with desired outcomes, consider restructuring the incentive component of bank teller compensation. Establish the appropriate level of performance measurement – whether at the firm, branch/team, or individual level. Determine if a variable pay program is justified given current salary levels and the potential award opportunity within the overall bank teller compensation framework.

-

Maintain Strong Governance for Performance and Costs: Implement robust risk review processes that encompass all incentive plans across the organization, including continuous monitoring and back-testing of retail incentive plans to ensure fair and compliant bank teller compensation practices.

Our latest Retail Pay Practices Study provides insights into trends from 50 U.S. banks. Contact our team to learn more about evolving retail banking compensation strategies and how they impact bank teller compensation.