Bank Transference is a ubiquitous term in finance, yet its intricacies often remain unclear, especially for businesses. While consumers may not frequently ponder the mechanics of bank transfers, understanding how they function is crucial for business owners. Knowing the timing, costs, and various types of bank transference is essential for effective financial management and offering diverse payment options to customers.

This article delves into the world of bank transference from a business perspective, providing the knowledge you need to navigate this essential payment method.

Article Contents:

- Defining Bank Transference

- Exploring Different Types of Bank Transference

- Debit Transfers (Bank Debits)

- Credit Transfers (Bank Credits)

- Bank Redirects

- Domestic Bank Transference Options in the U.S.

- ACH Transfers

- Wire Transfers

- International Bank Transference Networks

- CHAPS

- Bacs

- SEPA

- Bank Identifier Codes (BIC) Explained

- Advantages of Bank Transference for Businesses

- Disadvantages of Bank Transference for Businesses

- Security Aspects of Bank Transference

- Processing Times for Bank Transference

What is Bank Transference?

Bank transference, broadly defined, is the electronic movement of funds from one bank account to another. It’s an umbrella term encompassing various specific types of electronic fund transfers. Essentially, any electronic transfer of money between bank accounts can be considered a form of bank transference.

Types of Bank Transference

Bank transference methods can be categorized based on their operational geography and the network utilized for the transfer. Businesses commonly encounter three primary types of bank transference:

Bank Debits

Bank debits, also known as direct debits or debit transfers, occur when an account holder authorizes a third party to withdraw funds from their bank account. In this scenario, the transfer is initiated by the recipient’s bank, not the sender’s. When customers use this form of bank transference for payment, they provide their bank details to the payee. The payee then uses these details to instruct their bank to pull funds from the customer’s account.

In business-customer transactions, customers provide their bank account information to the business’s payment processor, granting authorization to debit the purchase amount. This method is commonly used for recurring payments and situations where the payer wants to grant the payee the authority to initiate withdrawals.

Bank Credits

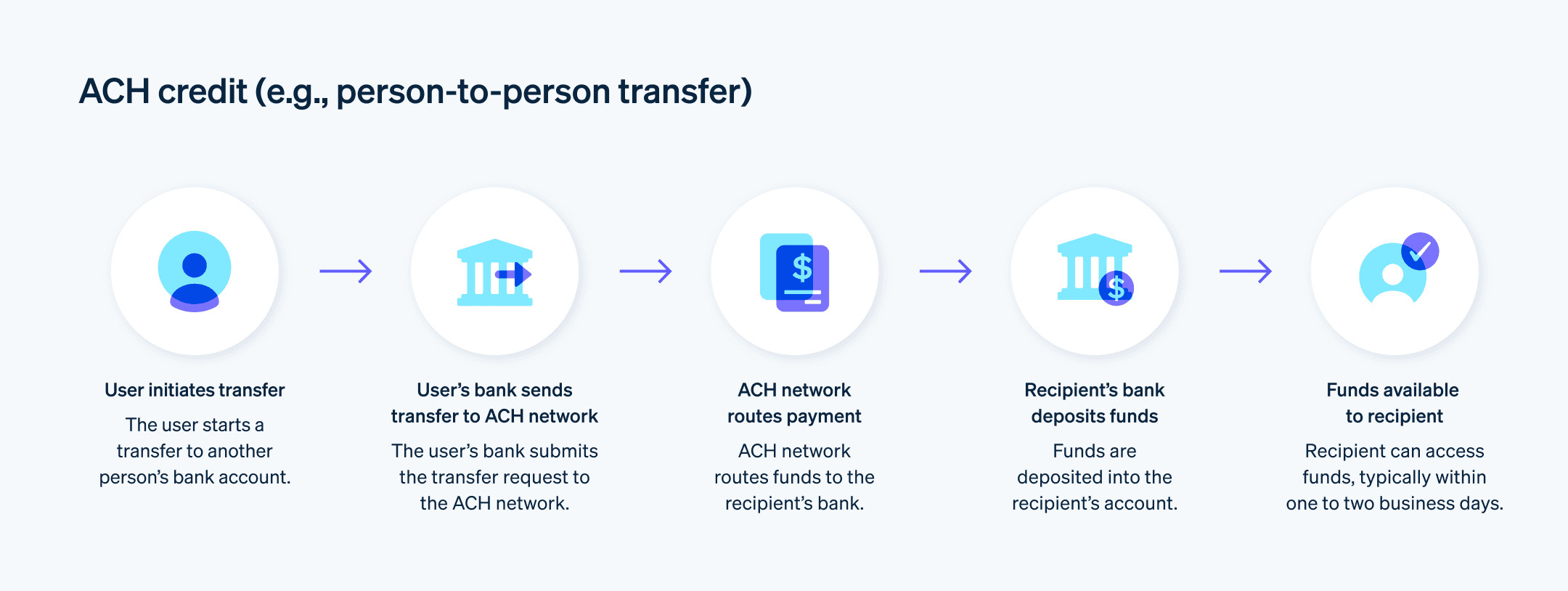

Bank credits, or credit transfers, operate on the same networks as debit transfers but with reversed action. Instead of the recipient’s account “pulling” funds, a credit transfer involves the sender’s bank “pushing” funds to the recipient’s bank account. This is the more traditional form of bank transference, often initiated by the payer.

Bank credits are initiated by the payer, who instructs their bank to send money to a specified recipient account. This method is widely used for one-time payments, supplier payments, and payroll.

ACH credit transfer flow chart – ACH credit transfer flow chart

ACH credit transfer flow chart – ACH credit transfer flow chart

Alt text: Flowchart illustrating the process of an ACH credit transfer, detailing steps from initiation by sender to receipt by receiver through the Automated Clearing House network.

Bank Redirects

Bank redirects are employed in specific online payment scenarios. Customers are redirected from the business’s website to their own financial institution’s online platform to authorize and complete the bank transference. This method is particularly popular for domestic online purchases in various countries. In fact, bank redirects are exceptionally prevalent in Europe and Asia-Pacific. For example, in Germany, the Netherlands, and Malaysia, bank redirects facilitate over half of all e-commerce transactions. Payment gateways like Stripe offer unified integrations supporting both domestic and international bank redirects, including popular services like Sofort and Giropay.

Here’s how bank redirects function within a payment flow using a provider such as Stripe:

- Customer Payment Selection: At checkout, the customer chooses “Bank Redirect” as their preferred payment method.

- Bank Selection: The customer selects their bank from a provided list of supported financial institutions.

- Redirection to Bank Website: The customer is securely redirected to their chosen bank’s online banking portal.

- Account Login: The customer enters their credentials to log into their online bank account.

- Authentication: The bank authenticates the login, often using two-factor authentication (2FA) such as SMS verification or mobile app approval.

- Payment Authorization: The customer reviews the payment details and authorizes the transaction with their bank.

- Payment Confirmation: The payment is processed and confirmed by the bank. The customer receives a notification of successful payment.

- Return to Merchant Website: The customer is redirected back to the business’s website, typically to an order confirmation page.

Domestic Bank Transference Options in the U.S.

In the United States, domestic bank transference primarily falls into two categories: ACH transfers and wire transfers. These methods operate through distinct networks with different characteristics and use cases.

ACH Transfers

ACH stands for Automated Clearing House. It’s a network managed by the National Automated Clearing House Association (Nacha), facilitating electronic funds transfers between banks and financial institutions across the U.S. Nacha is an independent organization owned by a consortium of banks, credit unions, and payment processors.

The ACH network operates on a batch processing system. ACH transactions initiated throughout the day (typically within roughly four-hour windows on business days) are accumulated and processed in batches at regular intervals. This batch processing makes ACH transfers cost-effective and efficient for high volumes of transactions.

ACH transfers are widely used for various commercial and non-commercial purposes, including:

- Customer bill payments

- Tax refunds from government agencies

- Tax payments to government agencies

- Retirement and investment account contributions

- Charitable donations

- Tuition payments for education

- Sending money to family and friends

There are two main types of ACH transfers, categorized by the direction of funds flow:

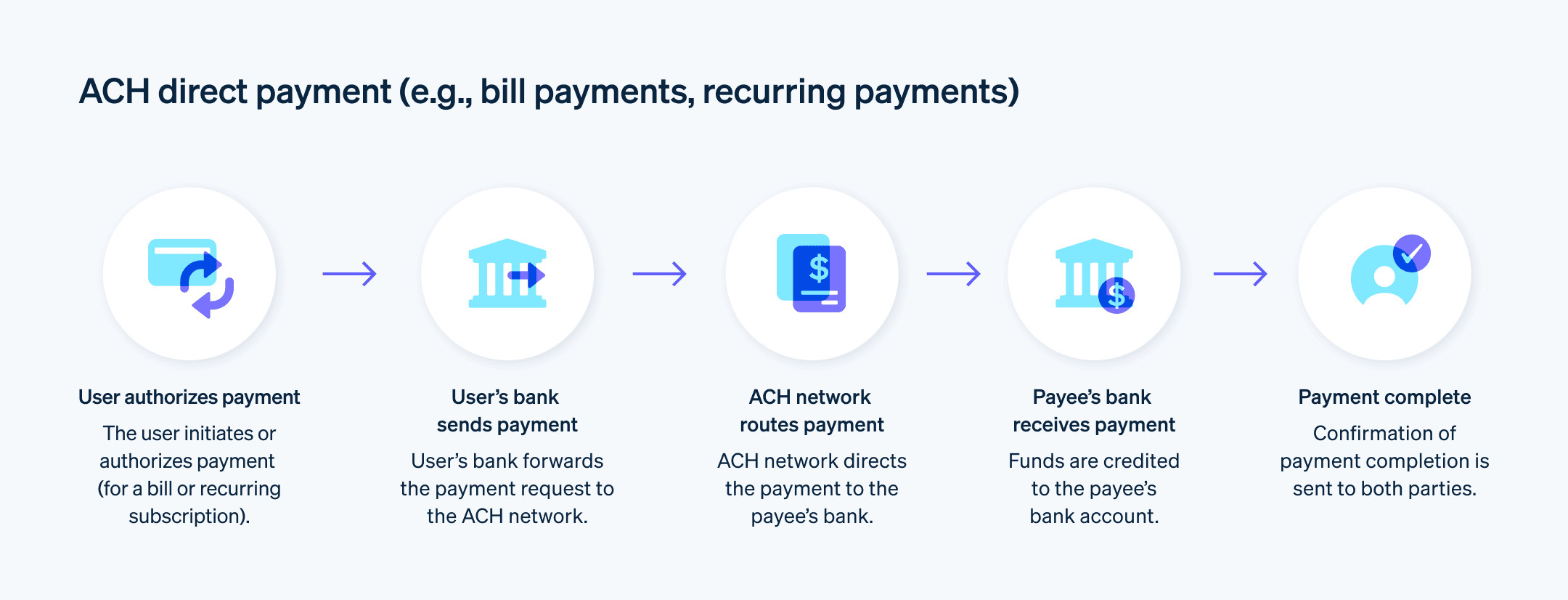

- ACH Debits (Direct Payments): Direct payments are initiated to pull funds from your account via the ACH network. These comprise the majority of non-payroll ACH transfers. For example, when a customer uses an ACH transfer to pay a business for goods or services, it’s typically an ACH debit or direct payment.

ACH direct payment flow chart – ACH direct payment flow chart

ACH direct payment flow chart – ACH direct payment flow chart

Alt text: Process flowchart of an ACH direct payment, showing the flow of information and funds from the payer to the payee via the ACH network and their respective banks.

- ACH Credits (Direct Deposits): Direct deposits are initiated to push funds into your account via the ACH network. Payroll direct deposits from employers are the most common example of ACH credits. Businesses also use ACH credits to pay vendors and suppliers.

Wire Transfers

Similar to ACH transfers, wire transfers facilitate fund movement between banks. However, while ACH transfers utilize the Nacha network, domestic wire transfers in the U.S. are processed through networks operated by the Federal Reserve. Unlike batch-processed ACH transfers, wire transfers are processed individually and in real-time. Historically, this has made them faster than ACH transfers, although recent regulatory updates by Nacha to expedite ACH processing are narrowing this gap.

Two primary wire transfer systems are supported by the Federal Reserve: the Federal Reserve Wire Network (Fedwire) and the Clearing House Interbank Payments System (CHIPS). These systems handle the majority of high-value domestic and international USD-denominated transactions.

- Fedwire: Fedwire is a real-time gross settlement (RTGS) system. It uses central bank money to electronically transfer funds between businesses, consumers, banks, and government entities. Fedwire is highly popular in the U.S., processing over 18 million transfers in March 2022 alone. Fedwire is favored for high-value, time-critical payments.

- CHIPS: Every financial market requires a clearinghouse to validate and finalize transactions between buyers and sellers. CHIPS (Clearing House Interbank Payments System) serves as the primary clearinghouse in the U.S. for large-value bank transference. The average CHIPS transfer exceeds $3 million USD, indicating its role in high-value corporate and interbank transactions.

International Bank Transference Networks

International bank transference between the U.S. and other countries predominantly relies on the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network. Established in 1973, SWIFT connects over 11,000 banks and financial institutions across more than 200 countries and territories. Governance of the SWIFT network is overseen by central banks from the G10 nations—Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom, and the United States.

Beyond the U.S., various countries utilize their own domestic systems for bank transference. Some notable examples include:

CHAPS

CHAPS (Clearing House Automated Payment System) is the UK’s equivalent to Fedwire. This network is used within the United Kingdom for same-day, high-value payments in British Pounds Sterling. CHAPS is essential for time-critical transactions within the UK financial system.

Bacs

Bacs (Bankers’ Automated Clearing Services) is an organization comprised of 16 of the UK’s leading banks and financial institutions. In 2020, Bacs processed 4.5 billion Direct Debit payments and approximately 2 billion Direct Credit payments. Bacs is a high-volume payment system primarily used for direct debits and payroll in the UK.

SEPA

SEPA (Single Euro Payments Area) is an integrated payment network designed to simplify euro-denominated bank transference within Europe. SEPA enables account holders in the EU/EEA countries and the UK to easily transfer funds between participating European banks. SEPA aims to create a harmonized and efficient payment landscape across Europe.

What are Bank Identifier Codes (BIC)?

Bank Identifier Codes (BICs) are standardized codes used to identify banks and financial institutions globally. A specific type of BIC, the SWIFT code, is essential for international bank transference and currency exchange within the SWIFT network. SWIFT/BIC codes ensure that international payments are routed correctly to the intended bank.

Advantages of Bank Transference for Businesses

Accepting bank transference as a payment method offers several key advantages for businesses:

No Chargebacks or Reversals

A significant benefit of bank transference is the elimination of chargebacks. Unlike credit card payments, which carry inherent chargeback risks, bank transfers, once initiated and completed, cannot be unilaterally reversed by the customer.

If a customer is dissatisfied after a bank transference payment, they must request a refund from the business. This process gives the business an opportunity to resolve the issue and potentially avoid a refund altogether. Even when a refund is necessary, it’s preferable to a chargeback, as businesses retain greater control over the refund process. Reduced chargebacks contribute to lower operational costs and improved revenue stability.

Enhanced Security

Bank transference is generally considered a highly secure payment method for businesses and customers alike. Compared to credit card payments, bank transfers present a lower risk of fraud. The authentication processes involved in bank transfers, particularly bank redirects, add layers of security.

Stripe users benefit from additional security measures for bank transference payments. Stripe provides virtual bank account numbers for customers to remit bank transfers. These virtual account numbers automate reconciliation and allow businesses to keep their actual bank account details confidential from customers, enhancing security and streamlining accounting processes.

Preferred Payment Method for Some Customers

It’s generally recommended that businesses offer a wide range of payment methods to cater to diverse customer preferences. Bank transference is particularly appealing to customers who prefer not to use credit or debit cards for certain purchases. Offering bank transference expands payment options and can attract customers who might otherwise not complete a purchase.

Higher Conversion Rates in Europe and Asia-Pacific

Bank transference is a dominant payment method in many European and Asia-Pacific markets. Accepting bank transference significantly increases appeal to customers in these regions who are accustomed to and prefer this payment method. For businesses targeting these markets, offering bank transference is crucial for maximizing conversion rates and achieving market penetration.

Disadvantages of Bank Transference for Businesses

While bank transference is a reliable, secure, and widely used payment method, it also presents certain disadvantages for businesses:

Limited Support for Recurring Payments

Bank transference, particularly bank credits, can be less ideal for recurring payments compared to direct debits or card-based subscriptions. Setting up automated recurring bank credit transfers can be complex and less user-friendly than other recurring payment methods. This can pose challenges for businesses relying on subscription models or installment payments.

Lack of Control Over Payment Amount

As bank credit transfers are often initiated by the customer, there’s a potential risk of incorrect payment amounts being transferred due to customer error. While safeguards can be implemented, such as payment reconciliation processes, discrepancies can still occur. Payment platforms like Stripe offer features to mitigate this, such as holding bank transfers, providing businesses with time (e.g., up to 90 days) to resolve discrepancies. However, investigating and rectifying incorrect payments still requires time and resources.

Risk of Incomplete Payments

The bank transference process can vary across financial institutions, making it challenging for businesses to provide universally applicable instructions to customers. Customers might believe they have completed a payment, when they may still need to finalize the transaction within their bank’s online system. Bank redirects largely mitigate this issue by guiding customers through the bank’s payment authorization flow. However, the risk of incomplete payments remains inherent to bank transference as businesses are ultimately reliant on the customer to fully complete the transaction process within their banking environment.

Higher Latency Risk

Bank transference networks can occasionally experience processing delays. Depending on the banks involved and the network used, funds may be held for several days. International transfers are even more susceptible to delays and holds due to increased scrutiny for fraud and compliance. While bank transference networks are continuously improving in speed and reliability, they generally have a higher latency risk compared to credit and debit card payments, which typically settle faster.

Is Bank Transference Secure?

Bank transference is generally considered a very secure method for businesses to accept payments, posing fewer risks compared to credit card payments. However, it’s important to note that consumers can be vulnerable to wire transfer scams. Educating customers about fraud prevention is important when offering bank transference as a payment option. From a business perspective accepting bank transference is secure and reliable.

How Long Do Bank Transfers Take?

Regardless of the sender or recipient, most bank transfers are processed and deposited within a few business days. Here’s a more detailed breakdown of processing times for different types of domestic and international bank transference:

USD Bank Transfers (ACH)

On March 19, 2021, Nacha operating rules were updated to expand same-day processing for the majority of ACH transactions. According to Nacha guidelines, USD-denominated ACH bank transfers typically deliver funds within one to two business days. ACH debits are generally required to settle by the next business day. However, some banks may place holds on funds transferred via ACH for a few days, depending on the financial institution’s policies.

Wire Transfers (Domestic)

Domestic wire transfers are processed in real-time and typically arrive within one business day, often within hours. However, initiating a wire transfer late on a Friday may result in funds not being available until the following Monday due to weekend processing schedules.

International Wire Transfers (SWIFT)

International SWIFT bank transfers between the U.S. and other countries usually take between one and five business days to complete. They take longer than domestic ACH and wire transfers due to increased compliance and security checks for fraud and money laundering prevention, as well as the involvement of multiple correspondent banks in the SWIFT network.

Disclaimer: The content of this article is intended for general information and educational purposes only and should not be construed as legal or tax advice. Stripe makes no representation or warranty as to the accuracy, completeness, or timeliness of any information contained in this article. You should consult with a competent legal counsel or tax advisor admitted to practice in your taxing jurisdiction for advice regarding your particular situation.