Are you puzzled by a mysterious charge on your bank statement and wondering How Do Bank Disputes Work? At bankprofits.net, we break down the bank dispute process, explaining how you can contest unauthorized or incorrect charges and potentially recover your funds, giving you more control over your financial well-being. Let’s unravel this process together, boosting your financial literacy and security with insights on payment disputes and financial reimbursements.

1. Understanding Bank Disputes: An Overview

1.1. What Exactly is a Bank Dispute?

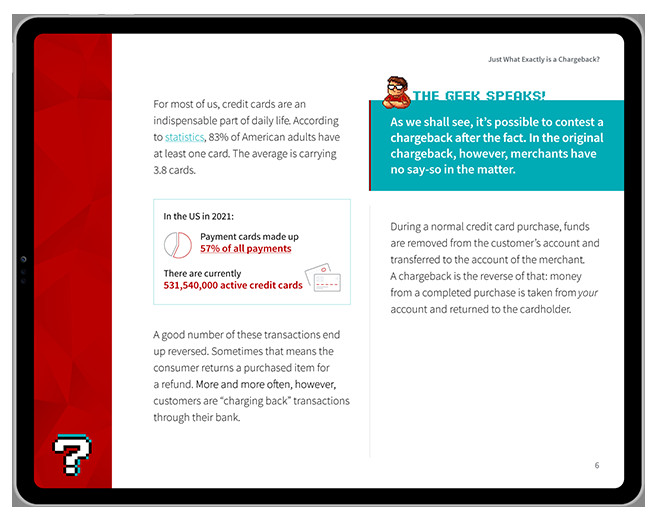

A bank dispute, also known as a chargeback, is a formal process initiated by a bank or credit union customer to contest a transaction on their account statement. This can occur when a customer believes there’s an error, unauthorized charge, or issue with the goods or services they paid for. According to the Consumer Financial Protection Bureau (CFPB), bank disputes are a critical tool for protecting consumers from fraudulent or erroneous transactions. This protection is essential in maintaining trust and security in the banking system.

1.2. Why are Bank Disputes Important?

Bank disputes play a vital role in safeguarding consumer rights and ensuring fair transactions. They provide a mechanism for resolving issues where merchants fail to deliver as promised or when fraud occurs. A study by the Federal Trade Commission (FTC) shows that disputes can recover substantial amounts for consumers annually, highlighting their significance in protecting personal finances. The ability to dispute charges ensures that customers are not held liable for unauthorized or incorrect transactions, fostering confidence in using electronic payment methods.

1.3. Who is Involved in a Bank Dispute?

The bank dispute process typically involves three main parties:

- The Cardholder (Consumer): The individual who initiates the dispute.

- The Bank (Issuer): The financial institution that issued the card or account to the cardholder.

- The Merchant (Retailer): The business that processed the transaction being disputed.

Each party has specific roles and responsibilities throughout the dispute process. The cardholder must provide accurate and timely information, the bank must investigate the claim, and the merchant has the right to present evidence supporting the transaction’s validity.

2. Reasons for Filing a Bank Dispute

2.1. Common Scenarios for Disputes

There are several valid reasons why a consumer might file a bank dispute. These include:

- Unauthorized Transactions: Charges the cardholder did not authorize or recognize.

- Billing Errors: Incorrect amounts charged, duplicate billing, or calculation errors.

- Non-Delivery of Goods or Services: Failure of the merchant to provide the promised goods or services.

- Defective Goods or Services: Goods or services that are not as described or are faulty.

- Fraudulent Activity: Instances where the cardholder’s account information has been stolen and used without permission.

Understanding these scenarios helps consumers recognize when a dispute is justified, ensuring they can protect their financial interests effectively.

2.2. Unauthorized Transactions: The Most Common Reason

Unauthorized transactions are one of the leading reasons for bank disputes. According to a report by the Nilson Report, unauthorized transactions account for a significant percentage of all credit card fraud. This can happen due to:

- Stolen Card Information: Data breaches or physical theft of the card.

- Online Hacking: Compromised online accounts or skimming devices.

- Phishing Scams: Deceptive practices to obtain personal and financial information.

Consumers need to monitor their account statements regularly and report any suspicious activity immediately to minimize potential losses.

2.3. Billing Errors: How to Spot and Dispute Them

Billing errors can take various forms, such as duplicate charges, incorrect amounts, or charges for services not rendered. Spotting these errors requires careful review of bank statements and transaction histories. Common billing errors include:

- Duplicate Charges: Being billed twice for the same purchase.

- Incorrect Amounts: Being charged a different amount than agreed upon.

- Subscription Issues: Charges continuing after a subscription has been canceled.

If you identify a billing error, it’s essential to gather supporting documentation, such as receipts or cancellation confirmations, and promptly file a dispute with your bank.

3. Step-by-Step Guide to Filing a Bank Dispute

3.1. Step 1: Contact Your Bank Immediately

The first step in filing a bank dispute is to contact your bank or credit union as soon as you notice the error or unauthorized charge. Most banks have a dedicated fraud department or customer service line for handling disputes. Prompt reporting increases the likelihood of a successful resolution and minimizes potential financial losses.

3.2. Step 2: Gather Supporting Documentation

Collecting relevant documentation is crucial for supporting your dispute claim. This may include:

- Transaction Receipts: Proof of purchase or payment.

- Contracts or Agreements: Terms of service or agreements with the merchant.

- Communication Records: Emails or letters exchanged with the merchant.

- Photos or Videos: Evidence of defective goods or services.

Providing detailed documentation strengthens your case and helps the bank investigate the issue more effectively.

3.3. Step 3: File a Formal Dispute Claim

After contacting your bank and gathering supporting documentation, the next step is to file a formal dispute claim. This typically involves completing a dispute form provided by the bank, either online or in person. The form will require you to provide details about the disputed transaction, the reason for the dispute, and any supporting evidence.

3.4. Step 4: Cooperate with the Bank’s Investigation

Once you’ve filed your dispute claim, the bank will initiate an investigation. Be prepared to cooperate with the bank by providing any additional information or documentation they may request. The bank may contact you or the merchant to gather further details about the transaction in question.

3.5. Step 5: Await the Bank’s Decision

After completing their investigation, the bank will make a decision on your dispute claim. This decision will be based on the evidence presented by both you and the merchant, as well as the bank’s internal policies and procedures. The bank will notify you of their decision in writing, typically within a specific timeframe outlined in their dispute resolution policy.

Woman Examining Bank Statement to File a Dispute

Woman Examining Bank Statement to File a Dispute

4. The Bank’s Investigation Process

4.1. How Banks Verify Disputes

Banks employ various methods to verify the legitimacy of disputes. These include:

- Reviewing Transaction Data: Examining transaction details such as date, amount, and merchant information.

- Contacting the Merchant: Seeking information and documentation from the merchant to support the transaction.

- Analyzing Customer History: Assessing the cardholder’s past transaction patterns and dispute history.

- Using Fraud Detection Tools: Employing software to identify potentially fraudulent transactions.

These verification methods help banks make informed decisions on dispute claims, balancing the need to protect consumers with the interests of merchants.

4.2. Gathering Evidence from the Merchant

As part of the investigation process, banks will often request information and documentation from the merchant involved in the disputed transaction. This may include:

- Sales Receipts: Proof of purchase or payment.

- Order Confirmations: Evidence that the customer placed an order.

- Shipping Records: Documentation showing that the goods were shipped and delivered.

- Service Agreements: Terms of service or contracts with the customer.

The merchant’s response and the evidence they provide play a crucial role in the bank’s decision-making process.

4.3. Timelines for Bank Investigations

The timelines for bank investigations can vary depending on the complexity of the dispute and the bank’s internal policies. According to the Electronic Funds Transfer Act (EFTA), banks generally have:

- Temporary Credit: Banks must provide provisional credit to the consumer’s account within 10 business days of receiving the dispute notice.

- Resolution Time: Banks must resolve the dispute within 45 days of receiving the notice. This can be extended to 90 days if the account is new (less than 30 days old).

These timelines ensure that disputes are resolved in a timely manner, protecting consumers from prolonged financial uncertainty.

5. Outcomes of a Bank Dispute

5.1. Dispute Resolved in Your Favor

If the bank resolves the dispute in your favor, you will typically receive a credit for the disputed amount. This credit may be temporary while the investigation is ongoing, or it may become permanent once the investigation is complete. The bank will also notify the merchant of the dispute and may take action against them if they are found to be at fault.

5.2. Dispute Resolved in Favor of the Merchant

If the bank resolves the dispute in favor of the merchant, the credit you received may be reversed, and you will be responsible for the disputed amount. This can happen if the bank determines that the transaction was valid, that you authorized the charge, or that the merchant provided the goods or services as agreed.

5.3. What to Do If You Disagree with the Bank’s Decision

If you disagree with the bank’s decision on your dispute claim, you have the right to appeal the decision. This typically involves submitting a written appeal to the bank, providing additional evidence or information to support your case. The bank will review your appeal and make a final determination.

Woman Celebrating Successful Bank Dispute Resolution

Woman Celebrating Successful Bank Dispute Resolution

6. How Merchants Can Handle Bank Disputes

6.1. Understanding the Merchant’s Perspective

From a merchant’s perspective, bank disputes can be costly and time-consuming. Each dispute can result in chargeback fees, loss of revenue, and damage to the merchant’s reputation. It’s essential for merchants to understand the dispute process and take steps to minimize disputes and protect their business.

6.2. Steps Merchants Can Take to Prevent Disputes

Merchants can take several steps to prevent bank disputes, including:

- Providing Excellent Customer Service: Addressing customer concerns promptly and professionally.

- Clearly Describing Products and Services: Providing accurate and detailed descriptions of goods and services.

- Ensuring Secure Transactions: Implementing security measures to protect customer data.

- Processing Refunds Quickly: Issuing refunds promptly when necessary.

- Monitoring Transactions for Fraud: Using fraud detection tools to identify suspicious activity.

These preventive measures can help merchants reduce the number of disputes they receive and maintain positive relationships with their customers.

6.3. Responding to a Dispute as a Merchant

When a merchant receives a notification of a dispute, it’s crucial to respond promptly and professionally. This involves:

- Reviewing the Dispute Details: Understanding the reason for the dispute and the customer’s claims.

- Gathering Supporting Evidence: Collecting documentation such as sales receipts, order confirmations, and shipping records.

- Submitting a Response to the Bank: Providing a detailed explanation of why the dispute is invalid and supporting it with evidence.

- Cooperating with the Bank’s Investigation: Providing any additional information or documentation requested by the bank.

By responding effectively to disputes, merchants can protect their revenue and minimize the negative impact on their business.

7. Bankprofits.net: Your Resource for Financial Insights

7.1. How Bankprofits.net Can Help

At bankprofits.net, we offer expert analysis, strategies, and up-to-date information to help you navigate the complexities of the banking industry. Whether you’re a banking professional, investor, or student, our goal is to provide you with the insights you need to succeed.

7.2. Featured Articles and Resources

Explore our extensive library of articles and resources, including:

- In-depth analyses of bank performance: Understand how banks are performing and the factors driving their success.

- Strategies for increasing bank profitability: Discover proven methods to improve your bank’s bottom line.

- Insights on industry trends: Stay ahead of the curve with our coverage of emerging trends in the banking sector.

- Tools for financial analysis: Access our calculators and templates to analyze bank financials.

7.3. Contact Us for Expert Consultation

Need personalized advice or consultation? Contact us at bankprofits.net. Our team of experts is ready to help you with your specific needs.

Address: 33 Liberty Street, New York, NY 10045, United States

Phone: +1 (212) 720-5000

Website: bankprofits.net

8. FAQs About Bank Disputes

8.1. How Long Does a Bank Dispute Take?

A bank dispute typically takes between 30 to 90 days to resolve, depending on the complexity of the dispute and the bank’s policies.

8.2. What Happens After I File a Dispute?

After you file a dispute, the bank will investigate the claim, gather evidence from both you and the merchant, and make a decision based on their findings.

8.3. Can a Merchant Fight a Dispute?

Yes, a merchant has the right to fight a dispute by providing evidence and documentation to support the validity of the transaction.

8.4. What Evidence Is Needed for a Successful Dispute?

Evidence needed for a successful dispute may include transaction receipts, contracts, communication records, and photos or videos.

8.5. What If I Don’t Have Proof of Purchase?

If you don’t have proof of purchase, you can still file a dispute, but it may be more challenging to win the case. Provide any other relevant information you have, such as the date of the transaction, the amount, and the merchant’s name.

8.6. Can a Bank Dispute Affect My Credit Score?

Filing a bank dispute typically does not directly affect your credit score. However, if the dispute involves non-payment of a debt, it could potentially impact your credit score.

8.7. What Is Friendly Fraud?

Friendly fraud is when a cardholder files a dispute for a legitimate transaction, often due to forgetting about the purchase or experiencing buyer’s remorse.

8.8. Can I Dispute a Cash Transaction?

Dispute processes are typically associated with electronic transactions. Cash transactions cannot be disputed through a bank.

8.9. What Is the Difference Between a Dispute and a Refund?

A dispute is a formal process initiated with your bank to contest a charge, while a refund is an agreement between you and the merchant to return the money for a purchase.

8.10. What Are My Rights as a Consumer?

As a consumer, you have the right to dispute unauthorized or incorrect charges, to receive a fair investigation of your claim, and to appeal the bank’s decision if you disagree with it.

9. Conclusion: Protecting Your Finances with Knowledge

Understanding how bank disputes work is essential for protecting your finances and ensuring fair transactions. By following the steps outlined in this guide, you can confidently navigate the dispute process and safeguard your financial well-being. At bankprofits.net, we are committed to providing you with the knowledge and resources you need to succeed in the world of finance.

Ready to take control of your financial security? Visit bankprofits.net today for in-depth analyses, effective strategies, and expert advice on bank profitability. Contact us to explore how we can assist you in understanding the intricacies of bank disputes, boosting your understanding of bank profits, and optimizing your financial strategies. Don’t wait—empower yourself with the knowledge you need to thrive!