Are you unsure how to accurately complete a bank deposit slip? This guide from bankprofits.net provides a simple, step-by-step approach to ensure your deposits are processed smoothly, maximizing your bank’s profitability and efficiency. Learn how to fill out a deposit slip, understand the role of key information, and discover insights into enhancing banking operations, all while exploring the benefits of strategic financial planning.

1. What is a Bank Deposit Slip and Why Is It Important?

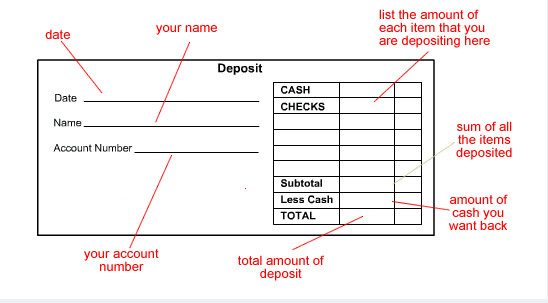

A bank deposit slip is a small form you fill out when depositing funds—cash, checks, or both—into your bank account at a branch. Its importance lies in ensuring that the money you’re depositing is correctly credited to your account. Think of it as a set of instructions for the bank teller, guiding them on where the money should go.

- Accuracy: A correctly filled deposit slip ensures that your funds are credited accurately and without delay.

- Record Keeping: The deposit slip acts as a physical record of your deposit, which can be useful for reconciling your accounts.

- Security: By providing clear instructions, you minimize the risk of errors and potential fraud.

2. What Information Do I Need Before Filling Out a Deposit Slip?

Before you start filling out a deposit slip, gather the following information to ensure accuracy:

- Your Full Name: This should match the name on your bank account.

- Your Account Number: This is essential for the bank to credit the funds to the correct account.

- Date: The current date is important for record-keeping.

- Cash Amount (if any): The total amount of cash you are depositing.

- Check Details (if any): The amount of each check and, ideally, the check number.

Having these details ready will streamline the process and reduce the chances of errors.

3. What Are the Key Sections of a Bank Deposit Slip?

Understanding the different sections of a bank deposit slip is crucial for filling it out correctly. Here’s a breakdown:

| Section | Description | Example |

|---|---|---|

| Date | The date of the deposit. | 2024-07-24 |

| Account Number | Your bank account number. | 1234567890 |

| Name | Your full name as it appears on the account. | John Doe |

| Cash | The total amount of cash being deposited. | $50.00 |

| Checks | A list of individual checks being deposited, including the amount of each check and, ideally, the check number. | Check 1: $100.00, Check 2: $50.00 |

| Subtotal | The sum of the cash and checks being deposited. | $200.00 |

| Less Cash Received | If you’re receiving cash back from the deposit, enter that amount here. | $20.00 |

| Total | The final amount being deposited after subtracting any cash received. | $180.00 |

| Signature (if required) | Some banks require a signature, especially if you’re receiving cash back or depositing a large amount. | John Doe |

Knowing what each section is for will help you complete the slip accurately.

4. How Do I Fill Out the “Cash” Section on a Bank Deposit Slip?

The “Cash” section is where you record the total amount of physical currency (bills and coins) you’re depositing. Here’s how to do it:

- Count Your Cash: Accurately count all the bills and coins you’re depositing.

- Write the Amount: Enter the total cash amount in the designated boxes. The box on the far right is for cents, and the box to the left is for the full dollar amount.

- Example: If you’re depositing $50.75 in cash, you would write “50” in the dollar box and “75” in the cents box.

If you’re not depositing any cash, leave this section blank.

5. How Do I List Checks on a Bank Deposit Slip?

When depositing checks, you need to list each one individually. Here’s how:

- Individual Lines: Each check gets its own line on the deposit slip.

- Check Amount: Write the amount of each check clearly.

- Check Number (Optional): Some deposit slips have a space for the check number. Including this can help with tracking and reconciliation.

- Additional Space: If you have more checks than lines on the front of the slip, use the back of the slip to continue listing them. Make sure to note that you’ve continued on the back.

For example, if you’re depositing two checks, one for $100 and another for $50, you would list them on separate lines with their respective amounts and check numbers.

6. What Is the “Less Cash Received” Section Used For?

The “Less Cash Received” section is used when you want to deposit money but also receive some cash back from the deposit. For example, if you’re depositing a $200 check but want $20 in cash, you would use this section.

- Enter the Amount: Write the amount of cash you want to receive in the “Less Cash Received” section.

- Calculate the Total: Subtract the “Less Cash Received” amount from the subtotal of your deposit to get the final deposit amount.

- Example: If your subtotal is $200 and you want $20 cash back, you would write $20 in the “Less Cash Received” section and $180 in the “Total” section.

Always double-check your math to ensure the final amount is correct.

7. How Do I Calculate the Subtotal and Total on a Bank Deposit Slip?

Calculating the subtotal and total accurately is crucial for ensuring your deposit is processed correctly. Here’s how:

- Subtotal: Add up the total amount of cash and checks you’re depositing. This is your subtotal.

- Less Cash Received (if applicable): If you’re receiving cash back, subtract that amount from the subtotal.

- Total: The result after subtracting any cash received from the subtotal is your final deposit amount.

Double-check your calculations to avoid any discrepancies.

8. Do I Need to Sign a Bank Deposit Slip?

Whether you need to sign a bank deposit slip depends on your bank’s policies and the type of transaction you’re making.

- Cash Back: Banks often require a signature if you’re receiving cash back from the deposit.

- Large Deposits: Some banks may require a signature for large deposits, regardless of whether you’re receiving cash back.

- Bank Policy: Check with your bank to understand their specific requirements for signing deposit slips.

If a signature line is provided, sign your name as it appears on your account.

9. What Happens After I Hand in My Deposit Slip to the Bank Teller?

After you hand in your deposit slip to the bank teller, here’s what typically happens:

- Verification: The teller will verify the information on the deposit slip and compare it to the funds you’re depositing.

- Processing: The teller will process the deposit, crediting the funds to your account.

- Receipt: You’ll receive a receipt as proof of your deposit. This receipt is an important record, so keep it in a safe place.

Always review the receipt to ensure the deposit amount is correct.

10. What Should I Do If I Make a Mistake on a Bank Deposit Slip?

If you make a mistake on a bank deposit slip, don’t panic. Here’s what you should do:

- Correct It: If the mistake is minor (like a small error in the cash or check amount), you can neatly cross out the incorrect information and write the correct information next to it. Initial the correction.

- Ask for a New Slip: If the mistake is significant or the deposit slip is too messy, ask the teller for a new one. It’s better to start fresh than to risk confusion.

- Explain the Situation: If you’ve already handed in the deposit slip and realize you made a mistake, inform the teller immediately. They can help correct the error.

Honesty and transparency are key when dealing with banking transactions.

11. Are There Alternatives to Using Bank Deposit Slips?

Yes, there are several alternatives to using traditional bank deposit slips:

- Mobile Deposits: Most banks offer mobile deposit services through their mobile app. You can deposit checks by taking a photo of them with your smartphone.

- ATM Deposits: Many ATMs allow you to deposit cash and checks without a deposit slip.

- Direct Deposit: For recurring payments like paychecks, you can set up direct deposit to have the funds automatically deposited into your account.

- Electronic Transfers: You can transfer funds electronically from another account.

These alternatives can save you time and effort compared to using deposit slips.

12. How Do Mobile Deposits Work and Are They Secure?

Mobile deposits have become increasingly popular due to their convenience. Here’s how they work and what you need to know about their security:

- How They Work:

- Open Your Bank’s App: Launch your bank’s mobile app on your smartphone.

- Select “Deposit”: Navigate to the deposit section.

- Enter the Amount: Input the amount of the check you’re depositing.

- Take Photos: Take a photo of the front and back of the check, following the app’s instructions.

- Submit: Review the information and submit the deposit.

- Security:

- Encryption: Banks use encryption to protect your data during transmission.

- Security Features: Mobile banking apps often have security features like biometric login and multi-factor authentication.

- Endorsement: Always endorse the back of the check with “For Mobile Deposit Only” and your signature to prevent fraud.

Mobile deposits offer a convenient and secure way to deposit checks from anywhere.

13. What Are the Advantages of Using Mobile Deposit Over Traditional Deposit Slips?

Mobile deposit offers several advantages over traditional deposit slips:

- Convenience: Deposit checks from anywhere, anytime, without having to visit a bank branch.

- Speed: Mobile deposits are often processed faster than traditional deposits.

- Accessibility: Accessible to anyone with a smartphone and a bank account.

- Reduced Paperwork: Eliminates the need for deposit slips and physical checks.

These advantages make mobile deposit an attractive option for many people.

14. What Is Funds Availability and Why Is It Important?

Funds availability refers to when you can actually access and use the money you deposit. It’s important because it affects when you can pay bills, make purchases, or withdraw cash.

- Bank Policy: Banks have funds availability policies that explain how long you need to wait to spend the money you deposit.

- Factors Affecting Availability: The type of deposit (cash, check, electronic transfer), the amount of the deposit, and your banking history can all affect funds availability.

- Regulation CC: In the United States, Regulation CC sets the standards for funds availability.

- Bank Five Nine Policy: Generally, Bank Five Nine makes funds from your deposit available to you on the first business day after the day we receive your deposit. Electronic direct deposits will be available on the day we receive the deposit.

Understanding funds availability is crucial for managing your finances effectively.

15. How Long Does It Typically Take for Funds to Become Available After a Deposit?

The time it takes for funds to become available after a deposit varies depending on several factors:

| Deposit Type | Availability Time |

|---|---|

| Cash | Typically available immediately. |

| Electronic Transfers | Often available on the same day or the next business day. |

| Local Checks | Usually available within one to two business days. |

| Non-Local Checks | May take longer, typically two to five business days. |

| Mobile Deposits | Availability can vary; some banks make funds available the next business day, while others may take longer. |

Always check with your bank to understand their specific funds availability policy.

16. What Are Some Common Reasons for Delays in Funds Availability?

Several factors can cause delays in funds availability:

- Large Deposits: Banks may place a hold on large deposits to verify the funds.

- New Accounts: New accounts may have longer hold times on deposits.

- Suspicious Activity: If the bank suspects fraud or other suspicious activity, they may delay the availability of funds.

- Non-Business Days: Deposits made on weekends or holidays may not be processed until the next business day.

- Check Type: Non-local checks or checks from accounts with a history of overdrafts may have longer hold times.

Understanding these factors can help you anticipate potential delays.

17. How Can I Check My Available Balance to Know When Funds Are Available?

Checking your available balance is the best way to know when funds are available. Here are several ways to do it:

- Online Banking: Log in to your bank’s website or mobile app to view your available balance.

- ATM: Check your balance at an ATM.

- Phone Banking: Call your bank’s customer service line to inquire about your balance.

- Bank Teller: Visit a bank branch and ask a teller to check your balance for you.

Choose the method that’s most convenient for you.

18. What Happens If I Try to Spend Money That Isn’t Available Yet?

If you try to spend money that isn’t available yet, you may incur overdraft fees or have your transaction declined.

- Overdraft Fees: If you try to make a payment or withdrawal that exceeds your available balance, your bank may charge an overdraft fee.

- Transaction Declined: The transaction may be declined, preventing you from making the purchase or withdrawal.

- Negative Balance: Your account may go into a negative balance, which can affect your credit score and your ability to open accounts in the future.

Avoid these issues by always checking your available balance before spending money.

19. How Can Banks Use Deposit Data to Improve Profitability?

Banks can leverage deposit data to gain valuable insights that can enhance their profitability in several ways:

- Customer Behavior Analysis: By analyzing deposit patterns, banks can understand customer behavior, such as deposit frequency, average deposit amount, and preferred deposit methods (e.g., mobile deposit, ATM, or in-branch).

- Personalized Marketing: Banks can use deposit data to tailor marketing campaigns to specific customer segments. For instance, customers with high deposit volumes might be targeted with premium banking services or investment opportunities.

- Optimizing Branch Operations: Analyzing deposit data can help banks optimize branch staffing levels and resource allocation. For example, if a branch experiences high deposit traffic during certain hours, the bank can ensure adequate staffing during those times.

- Fraud Detection: Monitoring deposit patterns can help banks identify and prevent fraudulent activities. Unusual deposit patterns, such as sudden large deposits or deposits from unfamiliar sources, can trigger alerts for further investigation. According to a report by the Federal Trade Commission (FTC), deposit account fraud has been on the rise, making robust fraud detection mechanisms crucial.

- Improving Funds Availability Policies: Banks can use deposit data to refine their funds availability policies. By understanding the risk associated with different types of deposits, banks can adjust hold times to balance risk management with customer convenience.

By effectively analyzing deposit data, banks can make informed decisions that improve operational efficiency, enhance customer relationships, and ultimately drive profitability.

20. What Role Does Technology Play in Modern Deposit Processing?

Technology plays a pivotal role in modern deposit processing, revolutionizing how banks handle deposits and enhancing efficiency, security, and customer experience.

- Automated Deposit Processing: Automated systems streamline deposit processing by reducing manual data entry and minimizing errors. These systems can automatically read and verify deposit slips, check amounts, and account information.

- Mobile Deposit Technology: Mobile deposit technology allows customers to deposit checks remotely using their smartphones, eliminating the need to visit a bank branch. This technology relies on image recognition and data encryption to ensure secure and accurate deposit processing.

- ATM Technology: Modern ATMs offer advanced deposit capabilities, allowing customers to deposit cash and checks without deposit slips. These ATMs use barcode scanners and image recognition technology to process deposits quickly and efficiently.

- Data Analytics: Banks leverage data analytics tools to analyze deposit data and gain insights into customer behavior, fraud detection, and operational efficiency. These tools can identify trends, patterns, and anomalies in deposit data, enabling banks to make informed decisions and optimize their operations.

Overall, technology has transformed deposit processing, making it faster, more efficient, and more convenient for both banks and customers.

21. How Do Regulations Impact the Deposit Process for Banks?

Regulations play a significant role in shaping the deposit process for banks, ensuring consumer protection, financial stability, and regulatory compliance.

- Regulation CC (Expedited Funds Availability Act): Regulation CC sets the standards for funds availability, requiring banks to make funds available to customers within specific timeframes. This regulation aims to ensure that customers have timely access to their deposited funds while allowing banks to manage risk.

- Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) Regulations: The BSA and AML regulations require banks to implement robust systems for detecting and preventing money laundering and other illicit financial activities. These regulations impact the deposit process by requiring banks to verify the identity of depositors, monitor deposit transactions for suspicious activity, and report large cash deposits to the government.

- Federal Deposit Insurance Corporation (FDIC) Regulations: The FDIC provides deposit insurance to protect depositors in the event of bank failure. FDIC regulations impact the deposit process by requiring banks to maintain adequate capital levels, adhere to sound banking practices, and provide clear disclosures to depositors about deposit insurance coverage.

- Consumer Financial Protection Bureau (CFPB) Regulations: The CFPB regulates consumer financial products and services, including deposit accounts. CFPB regulations impact the deposit process by requiring banks to provide clear and accurate disclosures about account fees, terms, and conditions, and to resolve consumer complaints in a timely and fair manner.

Adhering to these regulations is essential for banks to maintain regulatory compliance, protect consumers, and ensure the stability of the financial system.

22. Can You Provide Examples of How Bankprofits.net Can Help Financial Professionals With Deposit Strategies?

Bankprofits.net offers several resources and insights that can assist financial professionals in developing effective deposit strategies to enhance bank profitability and operational efficiency.

- Data-Driven Analysis of Deposit Trends: Bankprofits.net provides in-depth analysis of deposit trends, leveraging data from various sources to identify patterns and insights that can inform deposit strategies.

- Best Practices for Deposit Account Management: Bankprofits.net shares best practices for managing deposit accounts, including strategies for attracting and retaining depositors, optimizing deposit pricing, and managing deposit costs.

- Insights into Regulatory Compliance: Bankprofits.net offers insights into the regulatory landscape governing deposit accounts, helping financial professionals stay informed about regulatory changes and ensure compliance.

- Case Studies of Successful Deposit Strategies: Bankprofits.net features case studies of banks that have successfully implemented innovative deposit strategies. These case studies provide real-world examples and actionable insights that financial professionals can apply in their own organizations.

- Strategies for Leveraging Technology: Bankprofits.net explores how technology can be leveraged to enhance the deposit process, improve customer experience, and drive operational efficiency.

By providing access to these resources and insights, bankprofits.net empowers financial professionals to develop effective deposit strategies that drive profitability and sustainable growth.

23. What Emerging Trends Are Shaping the Future of Bank Deposits?

Several emerging trends are shaping the future of bank deposits, transforming how banks attract, manage, and utilize deposits to drive profitability.

- Digitalization of Deposits: The shift towards digital banking is accelerating, with more customers opting to manage their deposits online or through mobile apps.

- Rise of Fintech Competition: Fintech companies are disrupting the traditional banking landscape by offering innovative deposit solutions that compete with traditional bank accounts.

- Personalization of Deposit Products: Banks are increasingly personalizing deposit products to meet the unique needs and preferences of individual customers.

- Focus on Customer Experience: Banks are prioritizing customer experience in the deposit process, aiming to make depositing funds as easy, convenient, and seamless as possible.

- Emphasis on Data Analytics: Banks are leveraging data analytics to gain insights into deposit trends, customer behavior, and risk management.

- Integration of Blockchain Technology: Blockchain technology is being explored for its potential to enhance the security, transparency, and efficiency of the deposit process.

Staying informed about these emerging trends is crucial for banks to adapt their deposit strategies and remain competitive in the evolving financial landscape.

24. What Are Some Common Mistakes to Avoid When Filling Out a Bank Deposit Slip?

To ensure accurate and efficient deposit processing, it’s essential to avoid common mistakes when filling out a bank deposit slip.

- Inaccurate Account Number: An incorrect account number is one of the most common mistakes, leading to deposits being credited to the wrong account.

- Illegible Writing: Unclear handwriting can cause confusion and errors in processing the deposit.

- Incorrect Total: Miscalculating the total amount of the deposit can result in discrepancies and delays.

- Missing Information: Forgetting to include essential information, such as the date or signature (if required), can cause processing issues.

- Entering Cents Incorrectly: Failing to accurately enter the cents portion of the deposit can lead to errors in the deposit amount.

- Submitting Damaged Checks: Submitting checks that are torn, folded, or otherwise damaged can cause processing delays.

- Not Endorsing Checks: Forgetting to endorse checks with your signature and account number can result in the deposit being rejected.

Avoiding these common mistakes can help ensure that your deposits are processed quickly and accurately.

25. How Do Bank Deposit Slips Relate to Bank Profitability?

Bank deposit slips, while seemingly simple, play a crucial role in bank profitability. Here’s how:

- Operational Efficiency: Accurate and complete deposit slips streamline the deposit process, reducing the time and resources required to process each deposit. This operational efficiency translates into cost savings for the bank.

- Data Collection: Deposit slips provide valuable data about deposit activity, including deposit frequency, deposit amounts, and deposit methods. Banks can analyze this data to gain insights into customer behavior and optimize their deposit strategies.

- Customer Satisfaction: A smooth and hassle-free deposit process enhances customer satisfaction, which can lead to increased customer loyalty and retention. Loyal customers are more likely to use other bank services, such as loans and investments, which contribute to bank profitability.

- Fraud Prevention: Deposit slips can help banks detect and prevent fraudulent activities, such as check fraud and money laundering. By carefully reviewing deposit slips and monitoring deposit patterns, banks can identify suspicious transactions and take appropriate action to mitigate risk.

In summary, bank deposit slips are an integral part of the banking ecosystem, contributing to operational efficiency, data collection, customer satisfaction, and fraud prevention, all of which impact bank profitability.

26. What Resources Does the Federal Reserve Provide Regarding Bank Deposits?

The Federal Reserve System provides various resources and information related to bank deposits, including regulations, data, and educational materials.

- Regulation CC (Expedited Funds Availability Act): As mentioned earlier, Regulation CC sets the standards for funds availability, governing when banks must make deposited funds available to customers. The Federal Reserve publishes and enforces Regulation CC to ensure that banks comply with these standards.

- Data on Deposit Activity: The Federal Reserve collects and publishes data on deposit activity, including deposit balances, deposit growth rates, and deposit composition. This data provides valuable insights into the health of the banking sector and the overall economy.

- Educational Materials: The Federal Reserve offers educational materials on various topics related to bank deposits, including deposit insurance, funds availability, and consumer rights. These materials are designed to help consumers understand their rights and responsibilities when it comes to bank deposits.

- Research and Analysis: The Federal Reserve conducts research and analysis on various aspects of the banking industry, including deposit trends, deposit pricing, and the impact of regulations on deposit activity.

These resources provide valuable information and insights for banks, financial professionals, and consumers alike.

27. How Can Bankprofits.net Help Me Optimize My Bank’s Deposit Strategy?

Bankprofits.net is your go-to resource for optimizing your bank’s deposit strategy and boosting profitability. We provide:

- In-Depth Analysis: Our team of experts provides in-depth analysis of the latest deposit trends, regulatory changes, and competitive landscape.

- Actionable Strategies: We offer actionable strategies for attracting and retaining depositors, optimizing deposit pricing, and improving operational efficiency.

- Best Practices: We share best practices from leading banks around the world, helping you learn from their successes and avoid their mistakes.

- Data-Driven Insights: We leverage data analytics to provide you with data-driven insights into customer behavior, deposit patterns, and risk management.

- Customized Solutions: We offer customized solutions tailored to your bank’s specific needs and goals.

Visit bankprofits.net today to explore our resources and discover how we can help you optimize your bank’s deposit strategy and drive profitability. For personalized advice and in-depth analysis, contact us at +1 (212) 720-5000 or visit our office at 33 Liberty Street, New York, NY 10045, United States.

Example of cash and checks being prepared for a bank deposit.

Example of cash and checks being prepared for a bank deposit.

FAQ: Bank Deposit Slips

1. What is the purpose of a bank deposit slip?

The purpose of a bank deposit slip is to provide the bank teller with the necessary information to credit the correct account with the funds you are depositing.

2. Do I need a deposit slip if I’m depositing cash at an ATM?

Many modern ATMs allow you to deposit cash without a deposit slip. However, it’s always a good idea to check with your bank to confirm their ATM deposit procedures.

3. Can I use the same deposit slip for multiple accounts?

No, you should use a separate deposit slip for each account you are depositing funds into.

4. What should I do if I don’t have my account number memorized?

You can find your account number on your checks, bank statements, or by logging into your online banking account.

5. Is it safe to write my account number on a deposit slip?

Yes, it is generally safe to write your account number on a deposit slip, as this is necessary for the bank to credit your account. However, be sure to keep your deposit slip secure and avoid sharing it with unauthorized individuals.

6. Can I deposit a foreign check using a bank deposit slip?

Depositing a foreign check typically requires special handling and may not be possible using a standard bank deposit slip. Contact your bank for specific instructions.

7. What is the difference between a deposit slip and a withdrawal slip?

A deposit slip is used to deposit funds into your account, while a withdrawal slip is used to withdraw funds from your account.

8. Can I use a deposit slip to transfer money between my accounts at the same bank?

In most cases, you can use a deposit slip to transfer money between your accounts at the same bank. Simply fill out the deposit slip with the account you want to deposit into and indicate that the funds are coming from another account.

9. Are there any fees associated with using bank deposit slips?

No, banks typically do not charge fees for using bank deposit slips. However, you may be charged fees for other services related to your account, such as overdraft fees or monthly maintenance fees.

10. Where can I get bank deposit slips?

You can get bank deposit slips at your local bank branch, by ordering them online from your bank’s website, or by printing them from a template.