A bank number, also known as a routing number, is a crucial piece of information for anyone managing finances, and this article from bankprofits.net will explore its importance. It’s a nine-digit code that identifies your bank to ensure transactions are processed accurately and securely, playing a vital role in safeguarding bank profitability. Understanding this number can protect your assets and enhance your financial transactions.

1. Unveiling the Bank Number: Definition and Core Functions

What exactly is a bank number, and why is it so essential in the financial world? Let’s delve into the details to understand its significance.

1.1. Defining the Bank Number: A Comprehensive Overview

A bank number, most commonly referred to as a routing number, is a unique nine-digit code assigned to each financial institution. This number serves as an identifier, ensuring that funds are accurately routed during financial transactions. This is extremely crucial for maintaining profitability within the banking sector.

1.2. What are the Primary Functions of a Bank Number?

The primary function of a bank number is to facilitate the smooth and secure transfer of funds between banks. Here are some key functions:

- Identifying Financial Institutions: Bank numbers uniquely identify banks, credit unions, and other financial institutions.

- Facilitating Electronic Transfers: They are essential for electronic fund transfers (EFTs), including direct deposits, online bill payments, and Automated Clearing House (ACH) transactions.

- Processing Wire Transfers: Bank numbers are used to process both domestic and international wire transfers, ensuring that money reaches the correct destination.

- Ensuring Check Clearing: They are printed on checks to help clear them through the banking system efficiently.

- Supporting Secure Transactions: By accurately identifying financial institutions, bank numbers help prevent fraud and errors during financial transactions.

1.3. How Does the Bank Number Support Banking Profitability?

The efficiency and accuracy facilitated by bank numbers contribute directly to the profitability of banks. Here’s how:

- Reducing Transaction Errors: Accurate routing minimizes errors, reducing the costs associated with correcting mistakes.

- Streamlining Operations: Automated processes supported by bank numbers streamline banking operations, saving time and resources.

- Enhancing Customer Satisfaction: Secure and reliable transactions improve customer trust and loyalty, which are vital for long-term profitability.

- Facilitating Regulatory Compliance: Accurate transaction processing ensures compliance with financial regulations, avoiding costly penalties.

- Enabling Efficient Fund Management: Proper identification of financial institutions allows for better cash flow and liquidity management, essential for maintaining profitability.

1.4. What are the Key Components of a Bank Number?

The nine-digit bank number is divided into several parts, each serving a specific purpose:

- First Four Digits: These identify the Federal Reserve Routing Symbol, indicating which Federal Reserve Bank district the institution belongs to.

- Next Four Digits: These represent the ABA Institution Identifier, uniquely identifying the bank within its Federal Reserve district.

- Last Digit: This is the check digit, used to verify the accuracy of the routing number through a mathematical formula.

1.5. How to Find Your Bank Number

Finding your bank number is straightforward. Here are several methods:

- Check: The routing number is usually printed on the bottom left corner of your checks.

- Bank Statement: You can find your bank number on your bank statements, either paper or electronic.

- Online Banking: Log in to your bank’s online portal and navigate to your account details.

- Mobile App: Check your account information on your bank’s mobile app.

- Bank Website: Many banks provide a routing number lookup tool on their website.

- Customer Service: Contact your bank’s customer service and ask for your routing number.

ABA and Routing Number

ABA and Routing Number

Alt Text: Infographic illustrating where to locate the ABA routing number on a check, highlighting its position at the bottom left corner.

2. Why Is the Bank Number Important? Understanding the Significance

The bank number is more than just a string of digits; it is a critical component of the financial system. Its importance stems from its role in ensuring accuracy, security, and efficiency in financial transactions.

2.1. The Bank Number and Accuracy in Transactions

Accuracy is paramount in financial transactions, and the bank number plays a vital role in ensuring that funds reach the correct destination without errors.

- Avoiding Misdirected Funds: By uniquely identifying financial institutions, bank numbers minimize the risk of sending money to the wrong bank.

- Reducing Processing Delays: Accurate routing accelerates the processing of transactions, reducing delays and improving overall efficiency.

- Minimizing Transaction Errors: The check digit in the bank number helps verify its accuracy, further reducing the likelihood of errors.

2.2. The Bank Number and Security in Banking

Security is a top priority in the banking industry, and the bank number is an integral part of maintaining secure financial transactions.

- Preventing Fraud: By accurately identifying banks, bank numbers help prevent fraudulent activities, such as unauthorized transfers.

- Enhancing Authentication: Bank numbers are used in conjunction with other security measures to authenticate transactions and verify the identities of parties involved.

- Safeguarding Sensitive Information: Secure transaction processing protects sensitive financial information from being compromised during transfers.

2.3. The Bank Number and Efficiency in Financial Operations

Efficiency is key to the smooth operation of financial institutions, and the bank number contributes significantly to streamlining various processes.

- Automated Clearing House (ACH) Transactions: Bank numbers facilitate automated transactions, such as direct deposits and online bill payments, making them faster and more convenient.

- Wire Transfers: They are essential for processing wire transfers, both domestically and internationally, enabling quick and reliable money transfers.

- Check Clearing: Bank numbers help clear checks through the banking system efficiently, ensuring timely processing and fund availability.

2.4. The Bank Number and Regulatory Compliance

Regulatory compliance is crucial for banks to avoid penalties and maintain their operational licenses. Bank numbers support this by ensuring accurate transaction processing.

- Meeting Reporting Requirements: Accurate transaction data, facilitated by bank numbers, helps banks meet regulatory reporting requirements.

- Ensuring Transparency: Proper identification of financial institutions promotes transparency in financial transactions, aiding regulatory oversight.

- Avoiding Penalties: Compliance with transaction processing standards, supported by bank numbers, helps banks avoid costly penalties and legal issues.

2.5. The Bank Number and Customer Trust

Customer trust is essential for the success of any financial institution. Reliable and secure transactions, facilitated by accurate bank numbers, enhance customer confidence.

- Reliable Transactions: Accurate routing ensures that transactions are processed correctly and on time, enhancing customer satisfaction.

- Secure Fund Transfers: Secure processing protects customers’ money, reinforcing their trust in the bank.

- Efficient Services: Streamlined operations, supported by bank numbers, enable banks to provide efficient and convenient services, further strengthening customer relationships.

3. The Bank Number vs. The Account Number: Key Differences

It’s common to confuse bank numbers with account numbers. While both are essential for financial transactions, they serve different purposes. Understanding their differences is crucial for managing your finances effectively.

3.1. Defining the Account Number

An account number is a unique identifier assigned to each individual account held at a financial institution. It distinguishes your account from all others at the same bank, ensuring that transactions are correctly credited or debited.

3.2. What Is the Primary Function of an Account Number?

The primary function of an account number is to specify the exact account involved in a transaction. This ensures that money is deposited into or withdrawn from the correct account.

3.3. Key Differences Between Bank Number and Account Number

| Feature | Bank Number (Routing Number) | Account Number |

|---|---|---|

| Purpose | Identifies the financial institution | Identifies a specific account within that institution |

| Length | 9 digits | Varies, typically 8-12 digits |

| Uniqueness | Unique to each bank | Unique to each account within a bank |

| Usage | Used for bank-to-bank transactions | Used for transactions involving a specific account |

| Location on Check | Bottom left corner | Bottom middle |

| Examples of Use | Direct deposits, wire transfers, ACH transactions, check clearing | Crediting deposits, debiting withdrawals, online payments |

3.4. Why Understanding the Difference Matters

- Avoiding Transaction Errors: Knowing the difference between the two numbers helps ensure that you provide the correct information for transactions, reducing errors.

- Ensuring Accurate Fund Transfers: Providing both the correct bank number and account number is essential for accurate and timely fund transfers.

- Protecting Your Finances: Accurate transaction information protects your money from being misdirected or lost.

3.5. How to Use Both Numbers Correctly

- Double-Check Information: Always double-check both the bank number and account number before initiating a transaction.

- Use Reliable Sources: Obtain the numbers from reliable sources, such as your bank statement, checks, or online banking portal.

- Keep Information Secure: Protect your bank number and account number from unauthorized access to prevent fraud.

4. Common Uses of the Bank Number: Practical Applications

Bank numbers are used in a variety of financial transactions, each requiring accuracy and security. Understanding these common uses can help you manage your finances more effectively.

4.1. Direct Deposits: Receiving Payments Electronically

Direct deposit is a convenient way to receive payments, such as salaries, government benefits, and tax refunds, directly into your bank account.

- How It Works: Your employer or payer uses your bank number and account number to electronically deposit funds into your account.

- Benefits: Direct deposit is fast, reliable, and eliminates the need to handle paper checks.

- Example: When starting a new job, you provide your employer with your bank number and account number to set up direct deposit for your salary.

4.2. Online Bill Payments: Paying Bills Conveniently

Online bill payment allows you to pay your bills electronically through your bank’s website or mobile app.

- How It Works: You add your biller’s information, including their bank number and your account number with them, to your bank’s online system.

- Benefits: Online bill payment is convenient, saves time, and reduces the risk of late payments.

- Example: You set up online bill payment for your utility company by providing their bank number and your customer account number with them to your bank.

4.3. Automated Clearing House (ACH) Transfers: Electronic Fund Transfers

ACH transfers are electronic fund transfers between banks, used for a variety of purposes, including direct debits and credits.

- How It Works: ACH transfers involve the electronic movement of funds between bank accounts through the ACH network.

- Benefits: ACH transfers are efficient, secure, and cost-effective for recurring payments and transfers.

- Example: Setting up automatic payments for your mortgage or car loan involves ACH transfers, where funds are automatically debited from your account each month.

4.4. Wire Transfers: Sending Money Quickly

Wire transfers are a fast way to send money electronically, both domestically and internationally.

- How It Works: You provide the recipient’s bank number, account number, and other details to your bank, which then sends the money through the wire transfer system.

- Benefits: Wire transfers are quick and reliable, often used for large transactions and international transfers.

- Example: Sending money to a family member in another country may involve a wire transfer, requiring you to provide their bank number and account details.

4.5. Check Clearing: Processing Paper Checks

Check clearing is the process of transferring funds from the payer’s account to the payee’s account when a check is deposited.

- How It Works: The bank number printed on the check is used to identify the payer’s bank, and the check is processed through the banking system.

- Benefits: Check clearing allows for the transfer of funds from one account to another, even when using paper checks.

- Example: When you deposit a check into your account, the bank uses the bank number on the check to clear the funds from the payer’s account.

5. Locating Your Bank Number: A Comprehensive Guide

Finding your bank number is a straightforward process, but it’s essential to know where to look. Here are several reliable methods to locate your bank number.

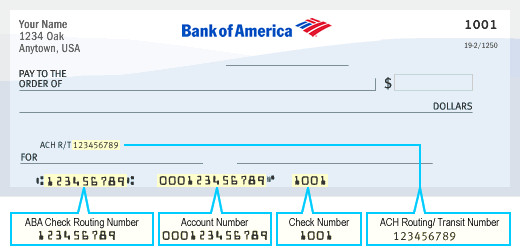

5.1. How to Find Your Bank Number on a Check

One of the easiest ways to find your bank number is on your checks. The routing number is typically printed on the bottom left corner of the check.

- Step-by-Step Instructions:

- Locate a check from your checkbook.

- Look at the bottom left corner of the check.

- Identify the nine-digit number; this is your bank number.

- Visual Aid: See the image above for a visual guide on where to find the bank number on a check.

5.2. How to Find Your Bank Number on a Bank Statement

Your bank statement, whether paper or electronic, also contains your bank number.

- Step-by-Step Instructions:

- Access your bank statement through online banking or review your paper statement.

- Look for the section that provides your account details.

- Find the nine-digit number labeled as “Routing Number” or “Bank Number.”

- Tips: Bank statements often include your bank number and account number for easy reference.

5.3. How to Find Your Bank Number Through Online Banking

Online banking portals provide convenient access to your bank number and other account details.

- Step-by-Step Instructions:

- Log in to your bank’s online banking portal.

- Navigate to your account summary or account details page.

- Look for the “Routing Number” or “Bank Number” section.

- Benefits: Online banking allows you to quickly access your bank number anytime, anywhere.

5.4. How to Find Your Bank Number Using a Mobile App

Many banks offer mobile apps that provide easy access to your account information, including your bank number.

- Step-by-Step Instructions:

- Open your bank’s mobile app on your smartphone or tablet.

- Log in to your account.

- Navigate to your account details or settings.

- Find the “Routing Number” or “Bank Number” section.

- Convenience: Mobile apps offer a convenient way to find your bank number on the go.

5.5. How to Find Your Bank Number on Your Bank’s Website

Some banks offer a routing number lookup tool on their website, allowing you to find your bank number by entering your account information.

- Step-by-Step Instructions:

- Visit your bank’s website.

- Look for a “Routing Number Lookup” or “Find Your Bank Number” tool.

- Enter the required information, such as your account number or location.

- Submit the form to retrieve your bank number.

- Accessibility: Bank websites provide an alternative way to find your bank number if you don’t have access to your checks or bank statements.

5.6. Contacting Customer Service

If you are unable to find your bank number through the methods above, you can contact your bank’s customer service for assistance.

- Step-by-Step Instructions:

- Call your bank’s customer service hotline.

- Verify your identity by providing the necessary information.

- Ask the customer service representative for your bank number.

- Direct Assistance: Customer service representatives can provide your bank number and answer any questions you may have.

6. Bank Number and Wire Transfers: A Detailed Look

Wire transfers are a fast and reliable way to send money electronically, both domestically and internationally. The bank number plays a crucial role in ensuring the accuracy and security of these transfers.

6.1. How Bank Numbers Facilitate Wire Transfers

Bank numbers are essential for directing wire transfers to the correct financial institution.

- Identifying the Receiving Bank: The bank number identifies the specific bank where the recipient’s account is held.

- Ensuring Accurate Routing: By accurately identifying the bank, the routing number ensures that the wire transfer reaches the intended destination without errors.

- Verifying Bank Details: The bank number is used to verify the details of the receiving bank, reducing the risk of fraud and misdirected funds.

6.2. Domestic Wire Transfers

Domestic wire transfers involve sending money electronically within the same country.

- Information Required: To initiate a domestic wire transfer, you typically need the recipient’s name, account number, bank number, and bank address.

- Process: Your bank uses the bank number to route the transfer to the recipient’s bank, where the funds are credited to their account.

- Speed: Domestic wire transfers are usually processed within 24 hours, making them a fast way to send money.

6.3. International Wire Transfers

International wire transfers involve sending money electronically to a bank in another country.

- Additional Information: In addition to the recipient’s name, account number, and bank number, you may need the SWIFT code or BIC code of the receiving bank for international transfers.

- SWIFT/BIC Code: The SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or BIC code (Bank Identifier Code) is a unique identifier for banks worldwide, used to facilitate international wire transfers.

- Process: Your bank uses the bank number and SWIFT/BIC code to route the transfer to the recipient’s bank, which then credits the funds to their account.

- Timeframe: International wire transfers can take several days to process, depending on the countries involved and the banks’ processing times.

6.4. Tips for Accurate Wire Transfers

- Verify Information: Always double-check the recipient’s bank number, account number, and other details before initiating a wire transfer.

- Use Reliable Sources: Obtain the information from reliable sources, such as the recipient or their bank.

- Confirm SWIFT/BIC Code: For international transfers, confirm the SWIFT/BIC code of the receiving bank to ensure accurate routing.

- Keep Records: Keep a record of the wire transfer, including the confirmation number and transaction details, for future reference.

6.5. Security Measures for Wire Transfers

- Secure Channels: Use secure channels for initiating wire transfers, such as your bank’s online portal or in-person at a branch.

- Authentication: Banks use various authentication methods to verify your identity before processing a wire transfer, such as passwords, security tokens, and biometric scans.

- Monitoring: Banks monitor wire transfers for suspicious activity and may contact you to verify the transaction before processing it.

7. Bank Number and ACH Transfers: Streamlining Electronic Transactions

Automated Clearing House (ACH) transfers are electronic fund transfers used for a variety of purposes, including direct deposits, online bill payments, and recurring payments. The bank number plays a vital role in facilitating these transactions.

7.1. How Bank Numbers Facilitate ACH Transfers

Bank numbers are essential for directing ACH transfers to the correct financial institution.

- Identifying the Banks Involved: The bank number identifies the sending and receiving banks in an ACH transfer.

- Ensuring Accurate Routing: By accurately identifying the banks, the routing number ensures that the ACH transfer reaches the intended destination without errors.

- Verifying Bank Details: The bank number is used to verify the details of the banks involved, reducing the risk of fraud and misdirected funds.

7.2. Types of ACH Transfers

- Direct Deposits: Employers use ACH transfers to deposit salaries directly into employees’ bank accounts.

- Online Bill Payments: Consumers use ACH transfers to pay bills electronically through their bank’s website or mobile app.

- Recurring Payments: Businesses use ACH transfers to collect recurring payments from customers, such as for subscriptions and memberships.

- Business-to-Business Payments: Companies use ACH transfers to pay suppliers, vendors, and other business partners.

7.3. The ACH Transfer Process

- Initiation: The payer initiates an ACH transfer by providing their bank number, account number, and the recipient’s bank number and account number to their bank.

- Transmission: The payer’s bank transmits the ACH transfer request to the ACH network, which is operated by the National Automated Clearing House Association (NACHA).

- Clearing: The ACH network clears the ACH transfer request and forwards it to the recipient’s bank.

- Settlement: The recipient’s bank credits the funds to the recipient’s account.

7.4. Benefits of Using ACH Transfers

- Efficiency: ACH transfers are efficient and cost-effective, reducing the need for paper checks and manual processing.

- Convenience: ACH transfers are convenient for both payers and recipients, allowing for automated and hassle-free transactions.

- Security: ACH transfers are secure, with various security measures in place to protect against fraud and unauthorized access.

- Reliability: ACH transfers are reliable, with a high success rate and minimal errors.

7.5. Security Measures for ACH Transfers

- Encryption: ACH transfers use encryption to protect sensitive information during transmission.

- Authentication: Banks use various authentication methods to verify the identities of parties involved in ACH transfers.

- Monitoring: Banks monitor ACH transfers for suspicious activity and may contact you to verify the transaction before processing it.

- Compliance: ACH transfers are subject to strict regulatory compliance requirements, ensuring a high level of security and reliability.

8. Potential Issues and How to Avoid Them: Ensuring Smooth Transactions

While bank numbers are designed to ensure smooth and accurate financial transactions, issues can arise if the information is incorrect or misused. Knowing potential problems and how to avoid them is crucial for protecting your finances.

8.1. Incorrect Bank Number: Consequences and Prevention

Providing an incorrect bank number can lead to significant problems, including delayed or misdirected transactions.

- Consequences:

- Delayed Transactions: Payments may be delayed if the bank number is incorrect, as the transaction cannot be processed until the correct information is provided.

- Misdirected Funds: Money may be sent to the wrong bank if the bank number is incorrect, potentially requiring significant effort to recover the funds.

- Failed Transactions: Transactions may fail if the bank number is invalid, requiring you to reinitiate the payment with the correct information.

- Prevention:

- Double-Check Information: Always double-check the bank number before initiating a transaction.

- Use Reliable Sources: Obtain the bank number from reliable sources, such as your bank statement, checks, or online banking portal.

- Verify with the Bank: If you are unsure about the bank number, contact your bank or the recipient’s bank to verify the information.

8.2. Fraudulent Use of Bank Numbers: Protecting Yourself

Fraudsters may attempt to use bank numbers for unauthorized transactions, such as identity theft and fraudulent payments.

- Risks:

- Unauthorized Transactions: Fraudsters may use your bank number to initiate unauthorized transactions from your account.

- Identity Theft: Your bank number may be used in conjunction with other personal information to commit identity theft.

- Phishing Scams: Fraudsters may attempt to obtain your bank number through phishing scams, posing as legitimate entities.

- Prevention:

- Protect Your Information: Keep your bank number and other personal information secure and do not share it with unauthorized parties.

- Be Wary of Phishing: Be cautious of suspicious emails, phone calls, or text messages asking for your bank number or other personal information.

- Monitor Your Accounts: Regularly monitor your bank accounts for unauthorized transactions and report any suspicious activity to your bank immediately.

- Use Secure Channels: Use secure channels for initiating financial transactions, such as your bank’s online portal or in-person at a branch.

8.3. Bank Number Changes: Staying Updated

Banks may occasionally change their bank numbers due to mergers, acquisitions, or other reasons. Staying updated on these changes is crucial for ensuring smooth transactions.

- Impact:

- Failed Transactions: Transactions may fail if you use an outdated bank number.

- Delayed Payments: Payments may be delayed if the bank number is no longer valid.

- Staying Updated:

- Bank Notifications: Banks typically notify customers of any changes to their bank numbers through email, mail, or online banking alerts.

- Check Bank Website: Check your bank’s website for updates on bank number changes.

- Contact Customer Service: Contact your bank’s customer service to confirm your bank number if you are unsure.

8.4. International Transactions: Additional Considerations

International transactions may involve additional complexities and potential issues related to bank numbers.

- SWIFT/BIC Codes: In addition to the bank number, international transactions often require the SWIFT code or BIC code of the receiving bank.

- Currency Conversion: Currency conversion fees and exchange rates may affect the amount of money received in international transactions.

- Regulatory Compliance: International transactions are subject to various regulatory compliance requirements, which may vary depending on the countries involved.

- Prevention:

- Verify SWIFT/BIC Code: Confirm the SWIFT/BIC code of the receiving bank to ensure accurate routing.

- Understand Fees: Be aware of any fees associated with international transactions, including currency conversion fees and transfer fees.

- Comply with Regulations: Comply with all regulatory requirements for international transactions, including reporting requirements and anti-money laundering regulations.

8.5. Reporting Issues: Taking Action

If you encounter any issues related to bank numbers, such as unauthorized transactions or misdirected funds, it’s essential to take action promptly.

- Contact Your Bank: Contact your bank immediately to report any unauthorized transactions or suspicious activity.

- File a Police Report: If you suspect fraud or identity theft, file a police report and provide your bank with a copy of the report.

- Monitor Your Credit Report: Monitor your credit report for any signs of identity theft and report any discrepancies to the credit bureaus.

- Change Your Passwords: Change your passwords for online banking and other financial accounts to prevent unauthorized access.

9. The Future of Bank Numbers: Innovations and Trends

The financial industry is constantly evolving, and innovations are emerging that may impact the use of bank numbers in the future. Understanding these trends can help you prepare for changes in how financial transactions are processed.

9.1. Digitalization of Banking: Impact on Bank Numbers

The increasing digitalization of banking is transforming how financial transactions are conducted, with a growing emphasis on electronic payments and digital wallets.

- Electronic Payments: Electronic payments, such as mobile payments and online transfers, are becoming more popular, reducing the need for paper checks and traditional bank numbers.

- Digital Wallets: Digital wallets, such as Apple Pay and Google Pay, allow you to store your payment information securely on your mobile device and make payments with a tap.

- Impact on Bank Numbers: While bank numbers are still used in some electronic payment systems, they may become less prominent as new technologies emerge.

9.2. Blockchain Technology: Potential Disruptions

Blockchain technology, which underlies cryptocurrencies like Bitcoin, has the potential to disrupt traditional banking systems and change how financial transactions are processed.

- Decentralized Transactions: Blockchain technology enables decentralized transactions, eliminating the need for intermediaries like banks and clearinghouses.

- Cryptocurrencies: Cryptocurrencies offer an alternative to traditional currencies, with transactions recorded on a public ledger using blockchain technology.

- Impact on Bank Numbers: If blockchain technology becomes more widely adopted, it could reduce the reliance on bank numbers for financial transactions.

9.3. Real-Time Payments: Faster Transactions

Real-time payments (RTP) systems allow for instant fund transfers between bank accounts, providing faster and more efficient transactions.

- Immediate Settlement: RTP systems offer immediate settlement of payments, reducing the time it takes for funds to become available in the recipient’s account.

- 24/7 Availability: RTP systems are available 24 hours a day, 7 days a week, allowing for instant payments at any time.

- Impact on Bank Numbers: While bank numbers are still used in RTP systems, the focus is on faster and more efficient transaction processing.

9.4. Enhanced Security Measures: Protecting Financial Data

As financial transactions become more digital, enhanced security measures are needed to protect against fraud and cybercrime.

- Biometric Authentication: Biometric authentication, such as fingerprint scans and facial recognition, is being used to verify identities and prevent unauthorized access to financial accounts.

- Multi-Factor Authentication: Multi-factor authentication requires you to provide multiple forms of identification, such as a password and a security code, to access your account.

- Encryption: Encryption is used to protect sensitive financial information during transmission and storage.

- Impact on Bank Numbers: Enhanced security measures help protect bank numbers from fraudulent use and ensure the integrity of financial transactions.

9.5. Regulatory Changes: Adapting to Innovation

Regulatory changes are needed to adapt to the rapid pace of innovation in the financial industry, ensuring that new technologies are safe, secure, and compliant with regulations.

- Data Privacy Regulations: Data privacy regulations, such as the General Data Protection Regulation (GDPR), aim to protect consumers’ personal information and ensure that it is used responsibly.

- Cybersecurity Regulations: Cybersecurity regulations require financial institutions to implement robust security measures to protect against cyber threats and data breaches.

- Anti-Money Laundering Regulations: Anti-money laundering regulations aim to prevent the use of financial systems for illicit purposes, such as money laundering and terrorist financing.

- Impact on Bank Numbers: Regulatory changes may impact how bank numbers are used and protected, requiring financial institutions to adapt their processes and systems.

10. FAQ: Addressing Common Questions About Bank Numbers

Understanding bank numbers can be complex, and many people have common questions about their use and importance. This FAQ section addresses some of the most frequently asked questions about bank numbers.

10.1. What is the difference between a bank number and a SWIFT code?

A bank number, also known as a routing number, is a nine-digit code used to identify banks within the United States. A SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or BIC code (Bank Identifier Code) is a unique identifier for banks worldwide, used to facilitate international wire transfers.

10.2. Can I use the same bank number for all my accounts at the same bank?

Yes, typically, all accounts at the same bank branch will share the same bank number. However, it’s always best to confirm the specific routing number for your account with your bank to avoid any issues.

10.3. What should I do if I suspect my bank number has been compromised?

If you suspect your bank number has been compromised, contact your bank immediately to report the issue. They can take steps to protect your account and prevent unauthorized transactions.

10.4. How often do bank numbers change?

Bank numbers do not change frequently. However, they may change due to bank mergers, acquisitions, or other reasons. Your bank will typically notify you if there are any changes to your bank number.

10.5. Is it safe to share my bank number?

It is generally safe to share your bank number with trusted parties for legitimate purposes, such as setting up direct deposit or online bill payments. However, be cautious of sharing your bank number with unknown or untrustworthy sources.

10.6. What is the purpose of the check digit in the bank number?

The check digit is the last digit in the nine-digit bank number. It is used to verify the accuracy of the bank number through a mathematical formula. This helps prevent errors during financial transactions.

10.7. Can I find my bank number online?

Yes, you can often find your bank number by logging into your bank’s online banking portal or mobile app. You can also check your bank’s website for a routing number lookup tool.

10.8. What is an ABA routing number?

ABA stands for American Bankers Association. An ABA routing number is the same as a bank number or routing number. It is a nine-digit code used to identify financial institutions in the United States.

10.9. How do I use a bank number for international wire transfers?

For international wire transfers, you typically need the SWIFT code or BIC code of the receiving bank, in addition to the bank number. Contact your bank for specific instructions on how to initiate an international wire transfer.

10.10. What are the alternatives to using bank numbers for financial transactions?

Alternatives to using bank numbers for financial transactions include electronic payment systems like PayPal, Venmo, and Zelle, as well as cryptocurrencies and blockchain technology.

Conclusion: The Indispensable Role of Bank Numbers

Bank numbers are indispensable for secure and efficient financial transactions. They ensure accurate routing, enhance security, and streamline operations, contributing to the stability and profitability of the banking system. Understanding the importance of bank numbers and how to use them correctly can protect your finances and enhance your financial transactions.

For more in-depth analyses, strategies, and insights on bank profitability, visit bankprofits.net. Our team of financial experts provides comprehensive information to help you navigate the complexities of the banking industry.

Ready to enhance your understanding of bank profitability and implement effective strategies? Explore our articles, analyses, and resources at bankprofits.net. Contact us today at 33 Liberty Street, New York, NY 10045, United States, or call +1 (212) 720-5000 for personalized guidance and support.