Paying by bank transfer is a common and convenient method for sending money, but how exactly does it work? This comprehensive guide from bankprofits.net will walk you through the process of making a bank transfer, highlighting key steps and potential considerations to ensure seamless and secure transactions that also help to improve bank profits. By understanding the nuances of bank transfers, you can optimize your financial strategies, enhance efficiency, and drive profitability within the banking sector.

1. What Is A Bank Transfer And Why Use It?

A bank transfer, also known as a wire transfer or electronic funds transfer (EFT), is a method of electronically moving funds from one bank account to another. It’s a secure and reliable way to send money, especially for larger amounts, and is widely used for various purposes, including:

- Paying Bills: Settling invoices, utility bills, and other recurring payments.

- Sending Money to Friends and Family: Transferring funds to loved ones, whether locally or internationally.

- Business Transactions: Paying suppliers, vendors, and employees.

- Investment Purposes: Funding brokerage accounts or making other investments.

- Real Estate Transactions: Transferring large sums of money for property purchases.

Bank transfers offer several advantages over other payment methods, such as cash or checks:

- Security: Bank transfers are generally considered more secure than other payment methods, as they involve electronic tracking and verification.

- Speed: While not always instantaneous, bank transfers are typically faster than sending checks or using other traditional methods.

- Convenience: You can initiate a bank transfer from the comfort of your home or office, using online banking or mobile apps.

- Traceability: Bank transfers provide a clear record of the transaction, making it easier to track payments and resolve disputes.

2. What Are The Different Types Of Bank Transfers?

There are several types of bank transfers, each with its own characteristics and use cases:

- Wire Transfers: Wire transfers are typically used for international transactions and involve a network of banks that facilitate the transfer of funds. They are generally faster but may also come with higher fees.

- Automated Clearing House (ACH) Transfers: ACH transfers are commonly used for domestic transactions, such as direct deposits and bill payments. They are generally slower and cheaper than wire transfers.

- Online Bank Transfers: Many banks offer online bank transfer services, allowing you to transfer funds between your accounts or to other accounts within the same bank or at other financial institutions.

- SWIFT Transfers: SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a global network that enables banks to securely send and receive information about financial transactions. SWIFT transfers are commonly used for international payments.

3. How Do You Initiate A Bank Transfer?

The process of initiating a bank transfer typically involves the following steps:

- Gather Recipient Information: You’ll need the recipient’s full name, bank name, account number, and routing number (for domestic transfers) or SWIFT code (for international transfers).

- Log In to Your Bank Account: Access your online banking portal or visit a bank branch.

- Navigate to the Transfers Section: Look for options like “Transfer Funds,” “Wire Transfer,” or “ACH Transfer.”

- Enter Recipient Details: Carefully enter the recipient’s information, ensuring accuracy to avoid delays or errors.

- Specify Transfer Amount: Indicate the amount you wish to transfer.

- Review and Confirm: Double-check all the details before confirming the transfer.

- Authorization: Depending on your bank’s security protocols, you may need to authorize the transaction using a one-time password (OTP) or other authentication method.

4. What Information Do You Need To Make A Bank Transfer?

To successfully complete a bank transfer, you’ll typically need the following information:

- Your Bank Account Details: Your account number and routing number.

- Recipient’s Full Name: The exact name as it appears on the recipient’s bank account.

- Recipient’s Bank Name: The name of the bank where the recipient holds the account.

- Recipient’s Account Number: The recipient’s unique bank account number.

- Recipient’s Routing Number (for Domestic Transfers): A nine-digit code that identifies the recipient’s bank.

- Recipient’s SWIFT Code/BIC (for International Transfers): An eight- or eleven-character code that identifies the recipient’s bank internationally.

- Recipient’s Address (for International Transfers): The recipient’s physical address.

- Purpose of Transfer (Optional): Some banks may require you to specify the reason for the transfer.

Providing accurate information is crucial to ensure that the transfer is processed smoothly and without delays.

5. What Are The Costs Associated With Bank Transfers?

Bank transfers often involve fees, which can vary depending on the type of transfer, the banks involved, and the amount being transferred. Here’s a breakdown of potential costs:

- Transfer Fees: Banks typically charge a fee for initiating a bank transfer. These fees can range from a few dollars to several hundred dollars, depending on the type of transfer and the bank’s fee structure.

- Recipient Fees: In some cases, the recipient’s bank may also charge a fee for receiving the transfer.

- Currency Conversion Fees: If you’re sending an international transfer, you may also be charged currency conversion fees. These fees can be a percentage of the transfer amount or a fixed fee.

- Intermediary Bank Fees: For international transfers, intermediary banks may also charge fees for processing the transaction.

It’s essential to compare fees from different banks and transfer services to find the most cost-effective option.

6. How Long Does A Bank Transfer Take?

The time it takes for a bank transfer to complete can vary depending on several factors:

- Type of Transfer: Domestic ACH transfers typically take 1-3 business days, while wire transfers can be completed within 24 hours. International transfers can take anywhere from 1-5 business days, depending on the countries involved and the banks’ processing times.

- Bank Processing Times: Some banks process transfers faster than others.

- Cut-off Times: Banks often have cut-off times for processing transfers. If you initiate a transfer after the cut-off time, it may not be processed until the next business day.

- Weekends and Holidays: Transfers are typically not processed on weekends or bank holidays, which can add to the overall processing time.

While some transfers can be completed within minutes, it’s always a good idea to allow for sufficient processing time, especially for international transactions.

7. Is It Safe To Pay Via Bank Transfer?

Bank transfers are generally considered a safe and secure method of payment, but it’s important to take certain precautions to protect yourself from fraud:

- Verify Recipient Information: Always double-check the recipient’s name, account number, and routing number before initiating a transfer.

- Use Secure Networks: When initiating a transfer online, make sure you’re using a secure network and that your computer is protected with up-to-date antivirus software.

- Be Wary of Scams: Be cautious of unsolicited requests for bank transfers, especially from unknown sources. Never provide your bank account information to someone you don’t trust.

- Monitor Your Account: Regularly monitor your bank account for any unauthorized transactions.

According to the Federal Trade Commission (FTC), consumers lost over $5.8 billion to fraud in 2021, with imposter scams and online shopping fraud being among the most prevalent types. Being vigilant and taking proactive steps can help you avoid becoming a victim of bank transfer fraud.

8. What Are The Pros And Cons Of Using Bank Transfers?

Like any payment method, bank transfers have their own set of advantages and disadvantages:

Pros:

- Security: Bank transfers are generally considered secure, with electronic tracking and verification.

- Convenience: You can initiate transfers online or at a bank branch.

- Traceability: Bank transfers provide a clear record of the transaction.

- Suitable for Large Amounts: Bank transfers are ideal for sending large sums of money.

Cons:

- Fees: Bank transfers can involve fees, especially for international transactions.

- Processing Time: Transfers may take several days to complete.

- Irreversible: Once a bank transfer is initiated, it can be difficult to reverse.

- Risk of Fraud: Although generally secure, bank transfers can be vulnerable to fraud if precautions aren’t taken.

9. How Do You Handle Disputes Or Errors With Bank Transfers?

If you encounter a problem with a bank transfer, such as an unauthorized transaction or an incorrect amount, it’s important to take action promptly:

- Contact Your Bank Immediately: Notify your bank as soon as you discover the error. They can investigate the issue and take steps to recover the funds.

- File a Dispute: Your bank may require you to file a formal dispute in writing.

- Gather Documentation: Collect any relevant documentation, such as transaction records or emails, to support your claim.

- Follow Up: Stay in contact with your bank and follow up on the progress of the investigation.

The Electronic Fund Transfer Act (EFTA) provides certain protections for consumers in the event of errors or unauthorized transfers.

10. What Are Some Alternatives To Bank Transfers?

While bank transfers are a popular payment method, there are several alternatives to consider:

- Debit Cards: Debit cards allow you to make purchases and payments directly from your bank account.

- Credit Cards: Credit cards offer a line of credit that you can use to make purchases and pay later.

- Payment Apps: Payment apps like PayPal, Venmo, and Zelle allow you to send and receive money electronically.

- Money Transfer Services: Services like Wise and Remitly specialize in international money transfers.

- Cash: Cash is a traditional payment method that can be used for in-person transactions.

The best payment method for you will depend on your specific needs and circumstances.

11. How Can Banks Optimize Profitability Through Effective Bank Transfer Management?

Effective management of bank transfers can significantly contribute to a bank’s profitability. Here are several strategies:

- Fee Optimization: Banks should strategically set transfer fees, balancing competitiveness with profitability. Analyzing transaction volumes and customer segments can help identify optimal fee structures. For instance, offering tiered pricing based on transfer frequency or amount can attract different customer groups.

- Operational Efficiency: Streamlining the transfer process reduces operational costs. Implementing automated systems for fraud detection, compliance checks, and transaction processing minimizes manual intervention and errors. This efficiency not only cuts costs but also improves customer satisfaction by speeding up transaction times.

- Customer Segmentation and Pricing: Different customer segments have varying needs and price sensitivities. Banks can offer tailored transfer services and pricing plans to maximize revenue. High-value customers might benefit from premium services with faster processing times and dedicated support, justifying higher fees.

- Technology Investment: Investing in advanced technology enhances transfer capabilities. Integrating blockchain for secure and transparent transactions, or AI-driven systems for predictive fraud analysis, can provide a competitive edge. These technologies improve security, reduce risk, and attract tech-savvy customers.

- Cross-selling Opportunities: Bank transfers provide opportunities for cross-selling other financial products. For example, customers making frequent international transfers might be interested in foreign currency accounts or investment products. Training staff to identify and capitalize on these opportunities can increase revenue.

- Compliance and Risk Management: Robust compliance and risk management practices are crucial. Banks must adhere to regulations like KYC (Know Your Customer) and AML (Anti-Money Laundering) to avoid penalties and maintain a strong reputation. Efficient compliance processes minimize delays and ensure smooth transactions.

- Partnerships and Alliances: Collaborating with other financial institutions and fintech companies can expand reach and service offerings. For example, partnering with remittance services can provide customers with more transfer options and competitive rates.

- Data Analytics: Utilizing data analytics to monitor transfer patterns, identify fraud risks, and understand customer behavior is essential. Analyzing transaction data can reveal insights into customer preferences, enabling banks to tailor services and marketing efforts.

- Customer Experience: Enhancing the customer experience is vital for retaining customers and attracting new ones. Providing user-friendly online platforms, mobile apps, and responsive customer support ensures a seamless transfer process. Positive experiences encourage repeat business and referrals.

- Security Measures: Implementing robust security measures protects against fraud and cyber threats. Multi-factor authentication, encryption, and real-time monitoring safeguard customer data and funds. Strong security protocols build trust and confidence in the bank’s transfer services.

By focusing on these strategies, banks can optimize their bank transfer operations to enhance profitability, improve customer satisfaction, and maintain a competitive edge in the financial industry. According to a report by McKinsey, banks that effectively leverage technology and data analytics can see a 20-30% increase in profitability.

12. What Role Does Technology Play In Modern Bank Transfers?

Technology has revolutionized modern bank transfers, making them faster, more secure, and more convenient. Here are some key technological advancements:

- Online Banking Platforms: Online banking platforms allow customers to initiate and manage bank transfers from their computers or mobile devices.

- Mobile Apps: Mobile banking apps provide a convenient way to send and receive money on the go.

- Real-time Payments: Real-time payment systems enable instant transfers between bank accounts.

- Blockchain Technology: Blockchain technology offers a secure and transparent way to record and verify bank transfers.

- Artificial Intelligence (AI): AI can be used to detect and prevent fraudulent bank transfers.

- Biometric Authentication: Biometric authentication methods, such as fingerprint scanning and facial recognition, enhance the security of bank transfers.

13. How Are Bank Transfers Regulated?

Bank transfers are subject to various regulations designed to protect consumers and prevent money laundering. Some key regulations include:

- The Electronic Fund Transfer Act (EFTA): The EFTA protects consumers who use electronic fund transfer services.

- The Bank Secrecy Act (BSA): The BSA requires banks to report suspicious activity and maintain records of large transactions.

- The USA PATRIOT Act: The USA PATRIOT Act strengthens anti-money laundering regulations and requires banks to verify the identity of their customers.

- The Dodd-Frank Act: The Dodd-Frank Act reforms the financial system and includes provisions related to bank transfers.

14. What Are The Implications Of International Bank Transfers?

International bank transfers involve additional considerations compared to domestic transfers:

- Currency Exchange Rates: Currency exchange rates can fluctuate, affecting the final amount received by the recipient.

- Fees: International transfers often involve higher fees than domestic transfers.

- Processing Time: International transfers may take longer to complete due to the involvement of multiple banks and countries.

- Regulations: International transfers are subject to different regulations depending on the countries involved.

- SWIFT Codes: International transfers require the use of SWIFT codes to identify the recipient’s bank.

15. How Can Businesses Streamline Bank Transfer Processes?

Businesses can streamline their bank transfer processes to improve efficiency and reduce costs:

- Automate Payments: Automate recurring payments to vendors and suppliers.

- Use Online Banking: Take advantage of online banking platforms to initiate and manage transfers.

- Integrate Accounting Software: Integrate your accounting software with your bank to automate reconciliation.

- Negotiate Fees: Negotiate with your bank to reduce transfer fees.

- Use a Payment Gateway: Use a payment gateway to process online payments securely.

Online bank transfers

Online bank transfers

Alt: Initiate online bank transfers by specifying amount and entering recipient’s details.

16. What Future Trends Will Shape Bank Transfers?

The future of bank transfers is likely to be shaped by several emerging trends:

- Increased Use of Real-time Payments: Real-time payment systems will become more widespread, enabling instant transfers between bank accounts.

- Adoption of Blockchain Technology: Blockchain technology will be used to enhance the security and transparency of bank transfers.

- Integration of AI and Machine Learning: AI and machine learning will be used to detect and prevent fraudulent bank transfers.

- Growing Popularity of Mobile Payments: Mobile payments will continue to grow in popularity, making it easier to send and receive money on the go.

- Focus on Customer Experience: Banks will focus on improving the customer experience by providing user-friendly online platforms and mobile apps.

17. What Are The Tax Implications Of Bank Transfers?

Bank transfers themselves are not typically taxable events. However, the underlying transactions that are funded by bank transfers may be subject to taxes. For example, if you’re using a bank transfer to pay for goods or services, sales tax may apply. Similarly, if you’re using a bank transfer to gift money to someone, gift tax may apply if the amount exceeds the annual exclusion limit.

According to the IRS, any single transaction or related transactions exceeding $10,000 must be reported. It’s always a good idea to consult with a tax advisor to understand the tax implications of your specific transactions.

18. How Do Bank Transfers Affect International Trade And Commerce?

Bank transfers play a crucial role in facilitating international trade and commerce. They allow businesses to make and receive payments for goods and services across borders. Without bank transfers, international trade would be much more difficult and costly.

The World Trade Organization (WTO) estimates that global trade is worth trillions of dollars annually. Bank transfers are the backbone of this trade, enabling businesses to participate in the global economy.

19. What Security Measures Should Be In Place When Making A Bank Transfer?

To ensure the security of your bank transfers, it’s important to take the following measures:

- Use Strong Passwords: Use strong, unique passwords for your online banking accounts.

- Enable Two-Factor Authentication: Enable two-factor authentication to add an extra layer of security to your accounts.

- Keep Your Software Up-to-Date: Keep your computer and mobile devices protected with up-to-date antivirus software.

- Be Wary of Phishing Scams: Be cautious of phishing emails and websites that try to trick you into providing your bank account information.

- Monitor Your Account Regularly: Regularly monitor your bank account for any unauthorized transactions.

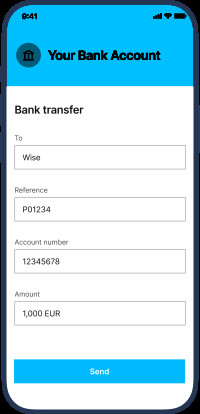

Alt: Choose your bank account to initiate a bank transfer.

20. How Do You Pay By Bank Transfer Using Wise?

Wise (formerly TransferWise) is a popular online platform that facilitates international money transfers. Here’s how to pay by bank transfer using Wise:

- Set up your transfer on Wise: Choose how much you’re sending and enter your recipient’s bank details.

- Choose bank transfer at the payment step: When you get to the payment step, choose bank transfer. This will bring up Wise’s bank account details, as well as a reference. Make a note of these — you’ll need them to pay with bank transfer through your bank.

- Leave your Wise account and pay by bank transfer directly through your bank: Pay by bank transfer directly through your bank either online, through your online banking, over the phone with your telephone banking, or in person at a bank branch, or by ATM with a cash card for JPY.

- You’re all done – wait for confirmation: Wise will send you an email as soon as your money arrives in Wise’s bank account. Then, they’ll convert it and pay it out to your recipient.

Important: To make sure that your transfer isn’t delayed, please double check that:

- The name on your bank account matches the name on your Wise account — if the names don’t match, Wise won’t be able to process your transfer. Wise can’t accept your deposit if you use someone else’s bank account with power of attorney to fund your transfer. But if you have a joint bank account, please see Wise’s help section for instructions.

- You’ve included the reference correctly — this helps Wise identify your deposit and proceed with your transfer.

- You enter the exact amount you’re sending with Wise — paying more or less could delay your transfer.

If you’re making a bank transfer from a UK bank, which is under the limit set by your bank, you may also see an option called Log in and approve. This is a faster and easier way of making an online bank transfer. If you choose that option, you’ll need to enter your online banking details, pick which account you’d like to pay from, and click approve. And that’s it — Wise does the rest.

FAQ: How Do You Pay By Bank Transfer?

1. What is a bank transfer?

A bank transfer is an electronic method of moving funds from one bank account to another, offering a secure way to send money, pay bills, or conduct business transactions.

2. What information do I need to make a bank transfer?

You’ll need the recipient’s full name, bank name, account number, routing number (for domestic transfers), or SWIFT code (for international transfers).

3. How long does a bank transfer take to complete?

Domestic ACH transfers typically take 1-3 business days, while wire transfers can be completed within 24 hours. International transfers can take 1-5 business days.

4. Are bank transfers safe?

Yes, bank transfers are generally considered safe, but it’s crucial to verify recipient information and use secure networks to protect against fraud.

5. What are the costs associated with bank transfers?

Costs can include transfer fees, recipient fees, currency conversion fees (for international transfers), and intermediary bank fees.

6. What should I do if there’s an error with my bank transfer?

Contact your bank immediately, file a dispute in writing, gather documentation, and follow up on the progress of the investigation.

7. Can I reverse a bank transfer after it’s been initiated?

It can be difficult to reverse a bank transfer once it’s initiated, so it’s crucial to double-check all details before confirming the transfer.

8. What are some alternatives to bank transfers?

Alternatives include debit cards, credit cards, payment apps like PayPal and Venmo, and money transfer services like Wise and Remitly.

9. How do international bank transfers differ from domestic ones?

International transfers involve currency exchange rates, higher fees, longer processing times, different regulations, and the use of SWIFT codes.

10. How can businesses streamline their bank transfer processes?

Businesses can automate payments, use online banking, integrate accounting software, negotiate fees, and use a payment gateway for secure online payments.

Paying by bank transfer is a reliable method to send funds, but requires attention to detail and security. By following these steps and understanding potential costs, you can make secure and efficient transfers.

For more in-depth analyses, strategies, and up-to-date information on bank profitability, visit bankprofits.net. Discover how to enhance your financial strategies, improve efficiency, and drive profitability in the ever-evolving banking sector. Contact us at Address: 33 Liberty Street, New York, NY 10045, United States. Phone: +1 (212) 720-5000, or visit our website at bankprofits.net for expert consulting services. Don’t miss out on the opportunity to elevate your bank’s performance and secure a prosperous future!

Bank Transfer New Design

Bank Transfer New Design

Alt: Verify bank transfer details to avoid delays and mistakes.